Health insurance policies are designed to cover hospitalization expenses, but no single base policy can cover every possible medical or financial risk. This is where riders in health insurance come into play.

In simple terms, riders are optional add-on benefits that you can attach to your existing health insurance policy by paying an additional premium. These riders enhance or customize your coverage based on your specific needs.

As healthcare costs continue to rise in India, understanding what riders are, how they work, and whether you actually need them has become essential for making an informed insurance decision.

What Are Riders in Health Insurance?

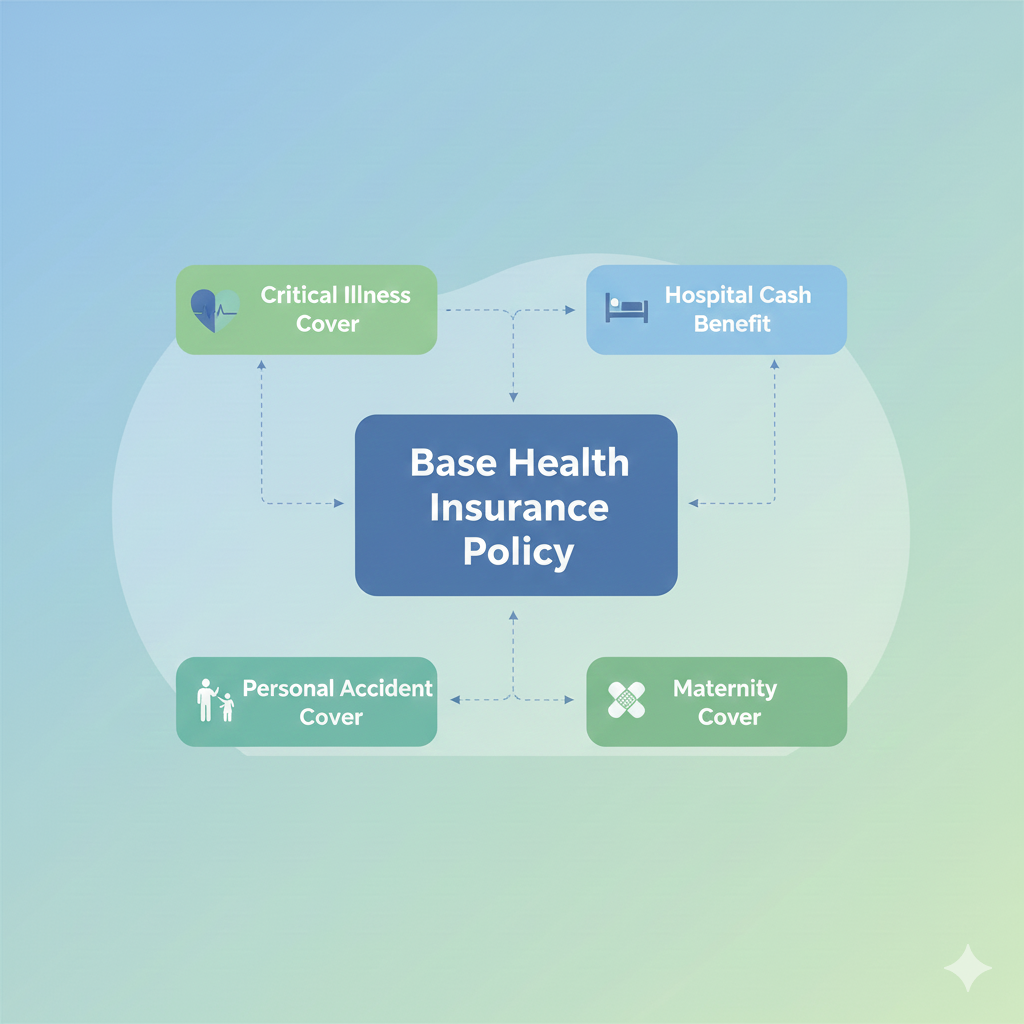

Riders in health insurance are supplementary benefits that extend the scope of coverage of a standard health insurance policy. They are not available as standalone plans and must be purchased along with a base health insurance policy.

Each rider covers a specific risk or expense that may not be fully covered under the main policy, such as critical illnesses, accidental disability, or hospital cash benefits.

Think of riders as customization tools that allow you to tailor your health insurance according to your life stage, lifestyle, and financial responsibilities.

Why Do Health Insurance Riders Exist?

Base health insurance policies are designed to remain affordable for the masses. To keep premiums reasonable, insurers limit coverage to hospitalization-related expenses.

Riders exist to:

- Cover non-hospitalization risks

- Provide lump sum payouts for specific conditions

- Reduce out-of-pocket expenses

- Address income loss during illness or disability

According to IRDAI data, medical inflation in India is estimated at 12–14% annually, which is significantly higher than general inflation. Riders help bridge the growing gap between actual medical costs and standard coverage limits.

How Do Riders in Health Insurance Work?

When you purchase a health insurance policy, insurers allow you to choose one or more riders by paying an additional premium. Once added:

- The rider remains active for the policy term

- Benefits apply only if rider-specific conditions are met

- Claims are settled as per rider terms, not base policy terms

Some riders pay a lump sum benefit, while others reimburse expenses or provide daily allowances.

💡 Important: Riders cannot exceed the sum insured of the base policy unless explicitly allowed.

Common Types of Riders in Health Insurance

1. Critical Illness Rider

This rider provides a lump sum payout if you are diagnosed with any illness listed in the policy, such as:

- Cancer

- Heart attack

- Stroke

- Kidney failure

The payout is independent of hospitalization bills and can be used for:

- Treatment costs

- Loss of income

- Lifestyle adjustments

2. Hospital Cash Rider

A hospital cash rider offers a fixed daily allowance for each day of hospitalization, regardless of actual expenses.

Example:

- ₹1,000–₹5,000 per day

- Paid for up to 30–60 days per year

This rider is useful for covering:

- Travel expenses

- Food for attendants

- Loss of daily wages

3. Accidental Disability Rider

This rider provides financial compensation in case of:

- Permanent total disability

- Permanent partial disability

- Accidental death (in some cases)

Given that road accidents account for over 4.5 lakh injuries annually in India (MoRTH data), this rider is particularly relevant for working professionals and daily commuters.

4. Room Rent Waiver Rider

Room rent capping is a common restriction in health insurance policies. A room rent waiver rider removes or relaxes this cap, allowing you to choose any hospital room without affecting claim settlements.

5. OPD Cover Rider

OPD (Outpatient Department) rider covers:

- Doctor consultations

- Diagnostic tests

- Pharmacy bills

As per industry estimates, over 60% of healthcare expenses in India are OPD-related, yet most base policies do not cover them.

6. Maternity Rider

Maternity riders cover:

- Normal and C-section deliveries

- Pre and post-natal expenses

- Newborn baby cover

These riders typically come with a waiting period of 2–4 years.

Benefits of Adding Riders to Your Health Insurance Policy

Enhanced Coverage Without Buying a New Policy

Instead of purchasing multiple policies, riders allow you to expand coverage within a single plan.

Cost-Effective Customization

Riders are generally cheaper than standalone policies offering similar benefits.

Better Financial Planning

Lump sum riders like critical illness help manage income loss and non-medical expenses.

Tailored to Life Stages

You can choose riders based on your:

- Age

- Marital status

- Family size

- Lifestyle risks

Riders vs Base Health Insurance: Key Differences

| Feature | Base Policy | Rider |

|---|---|---|

| Nature | Primary cover | Add-on benefit |

| Standalone purchase | Yes | No |

| Premium | Higher | Relatively lower |

| Coverage scope | Broad | Specific |

| Mandatory | Yes | Optional |

Are Health Insurance Riders Worth It?

Riders are worth considering if:

- You have limited savings

- You are the sole earning member

- Your employer health cover is insufficient

- You want protection beyond hospitalization bills

However, unnecessary riders can increase premiums without adding real value. Always assess your actual risk exposure.

Things to Check Before Buying Health Insurance Riders

Waiting Period

Many riders come with separate waiting periods.

Claim Conditions

Rider claims may have stricter definitions and exclusions.

Premium vs Benefit Value

Compare additional premium with the actual benefit payout.

Policy Compatibility

Not all riders are available with all policies.

Conclusion: Should You Add Riders to Your Health Insurance?

Health insurance riders are powerful tools when used wisely. They help bridge coverage gaps, manage indirect medical expenses, and provide financial stability during health emergencies.

Instead of blindly adding multiple riders, choose only those that align with your actual health risks and financial goals. A well-structured health insurance policy with the right riders can offer protection far beyond hospital bills.

Frequently Asked Questions (FAQs)

1. What are riders in health insurance in simple terms?

Riders are optional add-on benefits that enhance your health insurance coverage for specific risks by paying an extra premium.

2. Are health insurance riders mandatory?

No, riders are completely optional and can be chosen based on individual needs.

3. Can I add riders later to my existing policy?

Some insurers allow adding riders at renewal, while others require them at policy inception.

4. Do riders increase health insurance premium significantly?

Riders increase premiums marginally but are usually cost-effective compared to standalone covers.

5. Which rider is most important in health insurance?

There is no single best rider, but critical illness and hospital cash riders are commonly considered valuable.