Health insurance in India is often marketed as “affordable,” yet many policyholders feel premiums are rising faster than their salaries. A family floater policy that once cost ₹8,000–₹10,000 now easily crosses ₹25,000–₹40,000 per year.

So despite being a price-sensitive market, why is health insurance so expensive in India?

The answer lies in medical inflation, claim behavior, regulatory rules, and how insurers actually manage risk. Let’s break it down clearly.

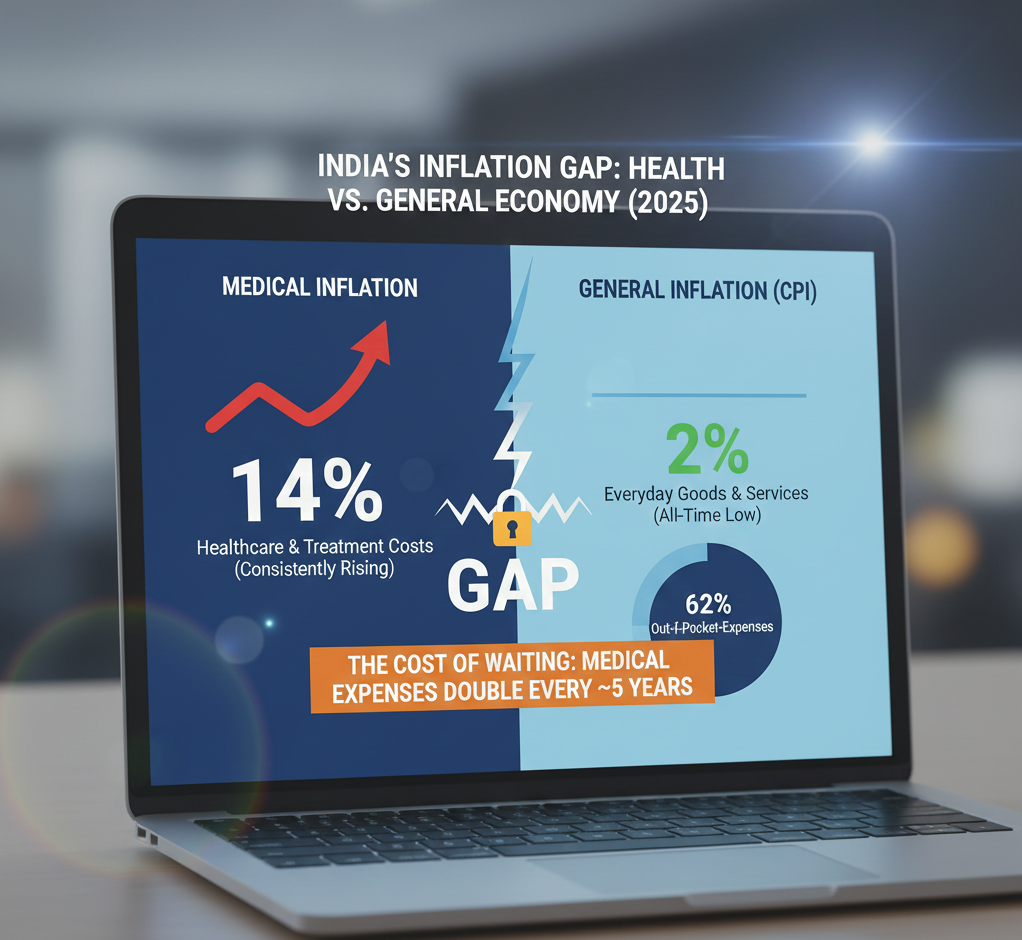

1. Medical Inflation in India Is Extremely High

One of the biggest drivers of expensive health insurance is medical inflation.

📈 How bad is it?

- India’s medical inflation: 12–15% annually

- General inflation: 5–6% annually

This means hospital bills double roughly every 5–6 years.

Why hospital costs are rising:

- Advanced diagnostic tests

- Expensive medical devices (often imported)

- Higher specialist doctor fees

- Corporate hospitals with hotel-like facilities

Insurers price premiums based on future hospital costs, not today’s prices — so premiums rise preemptively.

2. Hospitals Overcharge Insured Patients

This is uncomfortable but true.

Many hospitals follow dual pricing:

- Lower bills for cash-paying patients

- Higher bills for insured patients

Why this happens:

- Hospitals know insurers will negotiate later

- Room rent-linked billing inflates costs

- Unnecessary tests are bundled into insurance cases

💡 Example:

A surgery costing ₹1.5 lakh for a cash patient may become ₹3 lakh when insurance is involved.

👉 These inflated bills directly increase:

- Claim amounts

- Loss ratios

- Future premiums

3. Indians Buy Insurance Late (High-Risk Entry)

Unlike developed countries, most Indians:

- Buy health insurance after age 35–40

- Often after a medical condition is detected

Why this matters:

Insurance works best when healthy people pay premiums for many years.

But in India:

- Younger people avoid insurance

- Older, high-risk individuals dominate the pool

This leads to:

- More claims

- Higher payouts

- Expensive premiums for everyone

4. High Claim Rejection & Fraud Increases Premiums

Another hidden reason: claim misuse and fraud.

Common issues:

- Non-disclosure of pre-existing diseases

- Inflated hospital bills

- Fake hospitalizations

- Policyholders claiming immediately after buying insurance

When insurers lose money due to fraud:

They don’t absorb it — they spread the cost across future premiums.

Honest customers end up paying for dishonest behavior.

5. Regulatory Requirements by IRDAI

Insurance companies in India are tightly regulated by IRDAI (Insurance Regulatory and Development Authority of India).

Key rules affecting pricing:

- Mandatory coverage of pre-existing diseases after waiting periods

- No lifetime policy cancellation

- Limits on exclusions

- Standardized definitions

While these rules protect consumers, they also:

- Increase insurer liability

- Reduce pricing flexibility

Result: Higher premiums to balance long-term risk.

6. Reinsurance Costs Are Rising

Indian insurers don’t carry all risk themselves.

They transfer part of it to global reinsurers (companies that insure insurance companies).

Why reinsurance is expensive:

- Global medical costs are rising

- Pandemic-related losses (COVID aftermath)

- Currency fluctuations

When reinsurance becomes costly, Indian insurers pass that cost to customers.

7. Lifestyle Diseases Are Exploding

India is facing a silent epidemic of:

- Diabetes

- Hypertension

- Heart disease

- Obesity-related conditions

These are:

- Chronic

- Long-term

- Expensive to treat

A single diabetic policyholder may generate claims over decades, not years.

Insurers price this risk upfront — which increases premiums even for healthy individuals.

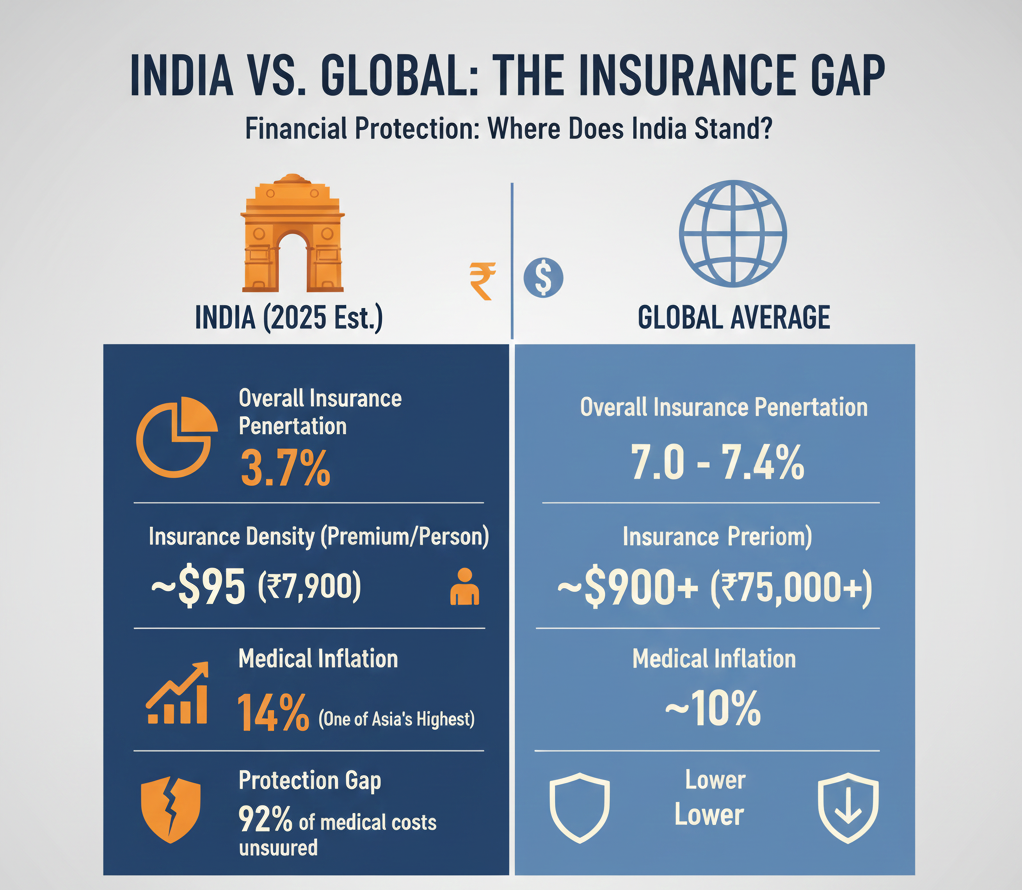

8. Low Penetration = Higher Cost Per Person

Health insurance penetration in India is still low when compared to the global average.

What this means:

- Smaller risk pool

- Fewer healthy people subsidizing sick ones

- Higher per-person cost

In countries with universal or near-universal coverage:

- Risk is spread widely

- Premiums remain stable

In India, insurance is still optional, making it costlier for those who buy it.

9. Frequent Policy Upgrades Increase Prices

Many people upgrade policies frequently:

- Higher sum insured

- Add-ons and riders

- Restoration benefits

- No-claim bonus boosters

While these are useful, they also:

- Increase insurer exposure

- Raise overall pricing levels

More benefits = higher premiums (there’s no free lunch).

10. Why Premiums Rise Every Year (Even Without Claims)

This confuses many policyholders.

Annual premium hikes happen because:

- Age-based risk increases

- Medical inflation adjustments

- Portfolio-level claim experience

- Regulatory changes

Even if you don’t claim, the risk group you belong to does.

Insurance is priced collectively, not individually.

Is Health Insurance Actually Expensive — Or Healthcare Is?

Here’s the uncomfortable truth:

Health insurance isn’t expensive. Healthcare is.

Insurance merely reflects:

- Hospital pricing

- Disease trends

- Consumer behavior

Without insurance, a single hospitalization can wipe out years of savings.

How to Reduce Health Insurance Cost (Smartly)

You can’t control the system — but you can control your strategy.

Practical tips:

- Buy early (before 30 if possible)

- Choose higher deductibles

- Avoid unnecessary add-ons

- Disclose all medical history honestly

- Stick with one insurer long-term

Final Thoughts

Health insurance in India feels expensive because it reflects real economic and healthcare realities, not because insurers are arbitrarily inflating prices.

As medical costs rise and lifestyles worsen, insurance will only become more important — not optional.

The smartest move is not avoiding insurance, but buying it early and using it wisely.

FAQs

1. Why do health insurance premiums increase every year in India?

Due to medical inflation, age-related risk, rising claims, and regulatory requirements.

2. Is private health insurance more expensive than government schemes?

Yes, but private insurance offers wider hospital networks, faster claims, and higher coverage flexibility.

3. Does having no claims guarantee lower premiums?

No. Premiums are based on group risk, not individual usage.

4. Why are family floater plans expensive?

Because multiple members increase the probability of at least one claim every year.

5. Will health insurance become cheaper in the future?

Unlikely, unless healthcare costs stabilize or insurance penetration improves significantly.