Switching jobs is exciting—but it also brings a wave of practical questions. One of the most common (and important) is: how does health insurance work when i switch jobs? or what happens to my health insurance when I change jobs?

In India, health insurance coverage can be a mix of employer-provided group insurance and your own individual policy. Understanding how these work together during a job switch can save you from coverage gaps, rejected claims, and loss of valuable benefits like waiting period credits.

This guide explains everything in simple terms so you can make informed decisions when transitioning between jobs.

How does health insurance work when i switch jobs?

Most salaried employees in India are covered under a group health insurance policy offered by their employer. These policies are negotiated by companies with insurers and usually provide:

- Coverage from day one of employment

- No medical tests

- Lower premiums (paid fully or partially by the employer)

- Coverage for dependents in many cases

However, these benefits come with a major limitation: the policy exists only as long as your employment does.

What Happens to Group Health Insurance When You Resign?

Once you leave your job:

- Your group health insurance policy typically expires on your last working day or shortly after

- Any claims after that date are not covered

- You lose accumulated benefits such as waiver of waiting periods

This is where most people get caught off guard—especially if there is a gap between jobs.

Health Insurance During the Job Switch Period

Scenario 1: Immediate Job Switch (No Gap)

If you move directly from one employer to another:

- Your old employer’s policy ends

- Your new employer’s group policy begins

- There is usually no overlap and no continuity between the two policies

While you remain insured, waiting periods may reset under the new group policy depending on its terms.

Scenario 2: Job Switch With a Gap

If there is a gap of weeks or months between jobs:

- You are completely uninsured unless you have a personal health insurance policy

- Any medical emergency during this period must be paid out of pocket

This is why relying only on employer-provided health insurance is risky.

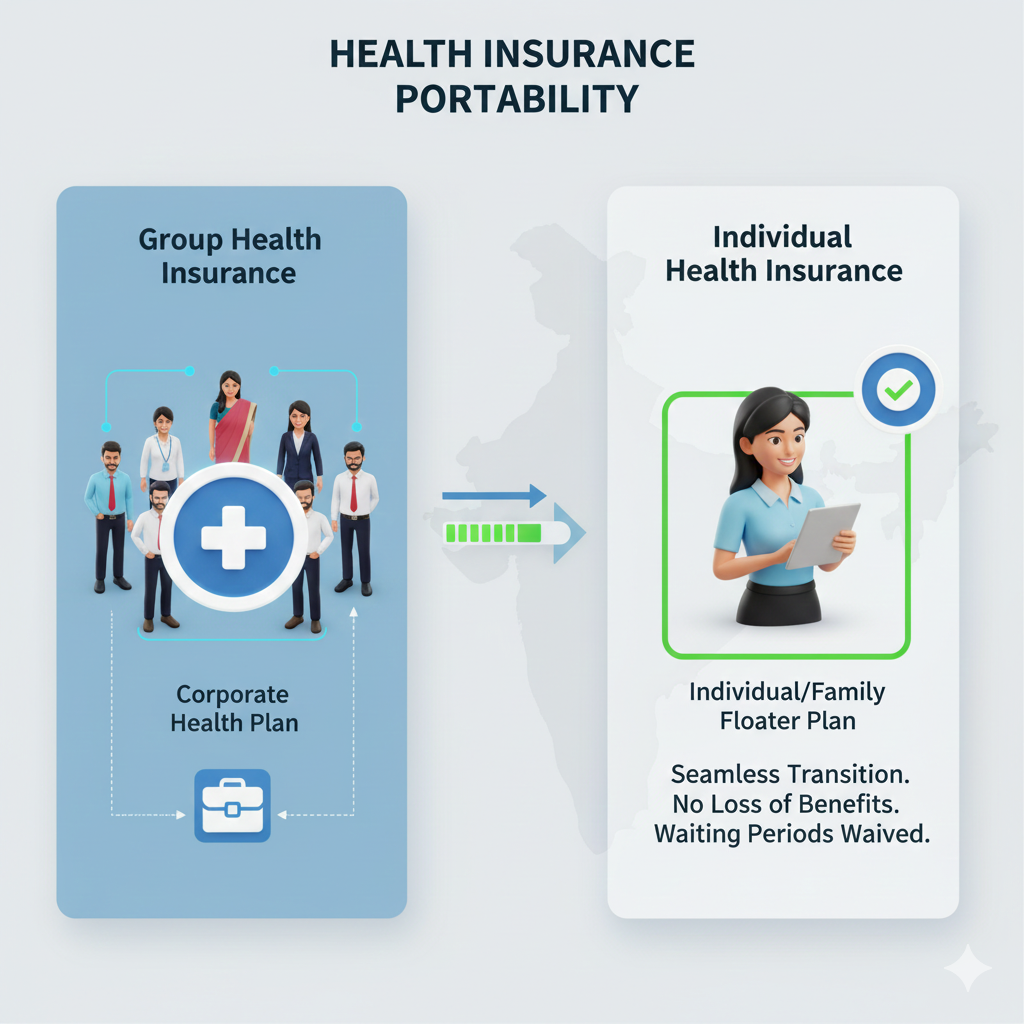

Can I Port My Employer Health Insurance Policy?

Yes—but with conditions.

Under IRDAI guidelines, employees can convert (port) their group health insurance policy into an individual health insurance plan when leaving a job.

How Group-to-Individual Portability Works

- You must apply for portability within a limited time window (usually 30–45 days from exit)

- Waiting period credits earned under the group policy can be carried forward

- Premiums will be higher than group insurance

- Coverage terms may differ from your old policy

Not all group policies are eligible, and not all insurers offer seamless conversion. This option is best used as a backup, not a primary strategy.

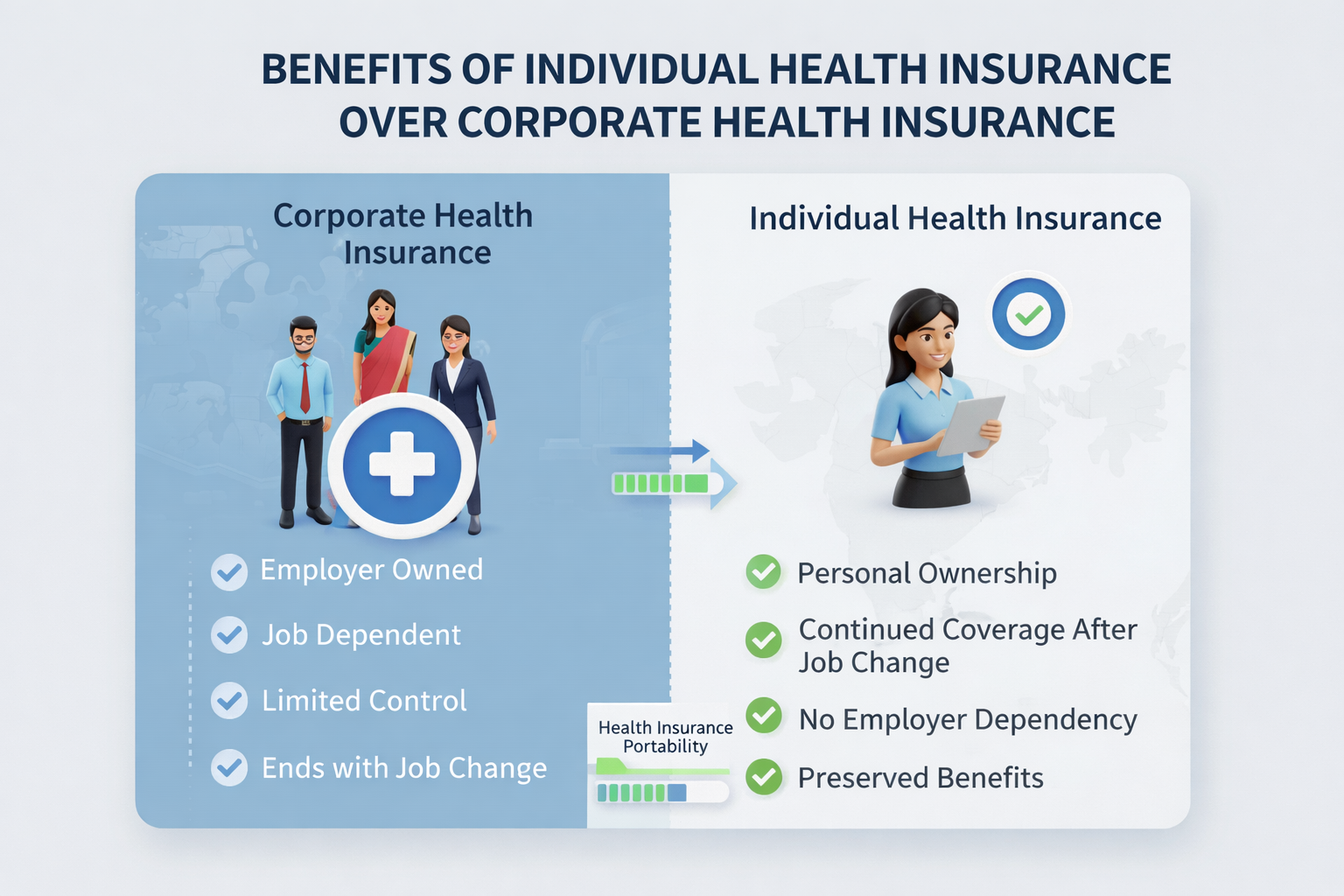

Role of Individual Health Insurance When Switching Jobs

An individual health insurance policy stays with you regardless of:

- Job changes

- Career breaks

- Switching industries

- Becoming self-employed

Why Individual Health Insurance Is Crucial

- Ensures uninterrupted coverage

- Protects waiting period benefits

- Offers long-term stability

- Provides flexibility to choose sum insured and add-ons

If you already have a personal policy, switching jobs has no impact at all on your coverage.

If you’re unfamiliar with why waiting periods matter, you can refer to our detailed guide on health insurance waiting periods.

What Happens to Waiting Periods When You Switch Jobs?

Waiting periods are one of the most misunderstood aspects of health insurance.

In Employer Health Insurance

- Waiting periods are often waived

- Pre-existing conditions may be covered immediately

- Benefits reset when you change employers

In Individual Health Insurance

- Waiting periods apply (initial, disease-specific, pre-existing)

- They continue uninterrupted as long as the policy is active

If you depend only on employer insurance, every job switch can effectively reset your benefits.

This is why experts recommend maintaining a personal policy alongside employer coverage.

What If My New Employer Has Better Health Insurance?

Even if your new employer offers:

- Higher sum insured

- Better hospital network

- Fewer sub-limits

…it should still be considered supplementary, not primary.

Employer policies can change every year based on:

- Company cost-cutting decisions

- Insurer changes

- Policy redesigns

You have no control over these changes.

Common Mistakes People Make While Switching Jobs

1. Assuming Employer Insurance Is Enough

Group policies are temporary by nature. Relying on them alone exposes you to risk.

2. Ignoring Coverage Gaps

Even a one-week gap without insurance can be financially disastrous during a medical emergency.

3. Losing Waiting Period Credits

Years of coverage benefits can be lost during job transitions.

4. Delaying Personal Policy Purchase

Buying health insurance at a younger age means:

- Lower premiums

- Shorter waiting periods

- Better acceptance

Best Strategy for Health Insurance When Switching Jobs

Here’s a smart, low-risk approach:

- Buy an individual health insurance policy early in your career

- Use employer health insurance as additional coverage

- Never let your personal policy lapse

- Increase sum insured gradually as income grows

This layered approach gives you continuity, flexibility, and financial security.

Regulatory Perspective in India

The Insurance Regulatory and Development Authority of India (IRDAI) allows:

- Portability of health insurance policies

- Transfer of waiting period credits under defined rules

You can review official guidelines on health insurance portability directly from IRDAI’s website for authoritative clarification.

For a broader understanding of how insurance principles work, concepts like risk pooling in health insurance also play a role in pricing and coverage stability.

Final Thoughts

Switching jobs is a normal part of career growth—but your health insurance strategy should remain stable. Understanding how employer and individual health insurance work during job transitions helps you avoid costly mistakes and ensures uninterrupted protection.

If there’s one takeaway, it’s this: your health insurance should be tied to you, not your employer.

Frequently Asked Questions (FAQs)

1. Does health insurance continue after I leave my job?

No. Employer-provided health insurance usually ends on your last working day or shortly after.

2. Can I keep my employer health insurance after resignation?

Only by converting it into an individual policy, subject to insurer rules and timelines.

3. Will my waiting period reset when I switch jobs?

Yes, employer health insurance waiting period benefits typically reset with a new employer.

4. Is individual health insurance affected by job change?

No. Individual health insurance stays active regardless of employment status.

5. Is it safe to rely only on company health insurance?

No. Employer health insurance should be treated as temporary and supplementary coverage.