Health insurance is one of the most important financial safety nets you can have, especially in India where medical costs are rising rapidly. But many first-time buyers find themselves puzzled by waiting periods — the time you must wait before certain coverages become active.To make better decisions, avoid unexpected gaps, and choose smarter policies, you must understand why health insurance has waiting periods?

In this article, we’ll explain what waiting periods are, why they exist, how they affect your coverage, and what you can do to manage them effectively.

What Is a Waiting Period in Health Insurance?

A waiting period is a specific duration during which a health insurance policy will not cover certain illnesses, conditions, or treatments — even if you’ve paid your premiums on time.

Types of Waiting Periods

Waiting periods typically fall into a few categories:

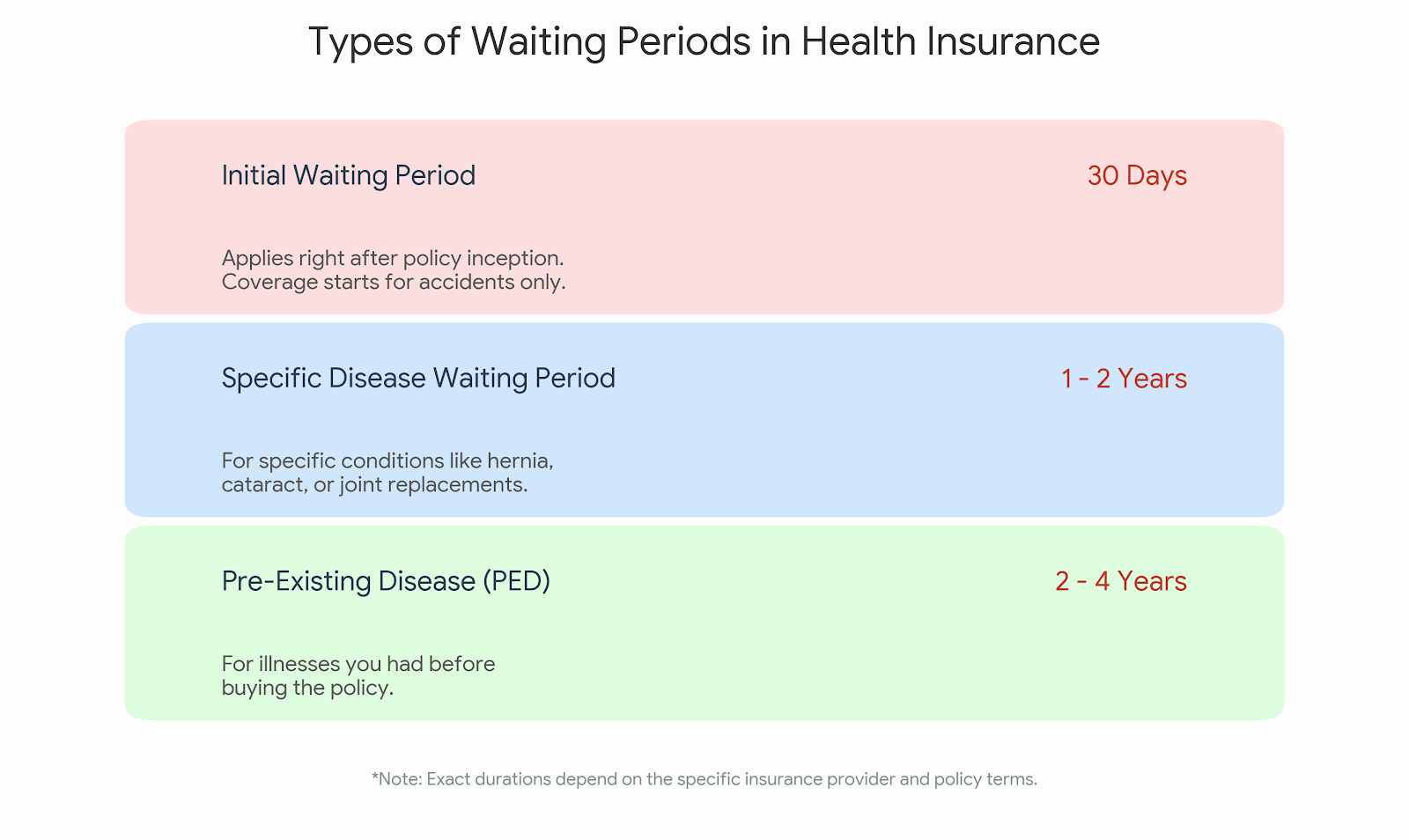

Initial Waiting Period

Applies right after policy inception (often 30 days)

Pre-Existing Disease (PED) Waiting Period

For conditions you had before buying the policy (usually 2–4 years)

Specific Disease Waiting Period

For conditions like hernia or joint replacements (1-2 years. Although it varies by insurer)

These waiting periods are regulated by the Insurance Regulatory and Development Authority of India (IRDAI), which sets minimum standards for how waiting periods should be applied. You can read more about IRDAI guidelines on their official site ➡️ https://www.irdai.gov.in

—

Why Health Insurance Has Waiting Periods (The Full Explanation)

Waiting periods exist for several sound reasons, both economic and practical. Understanding them helps you see health insurance as a long-term risk-sharing product, not just a quick payout tool.

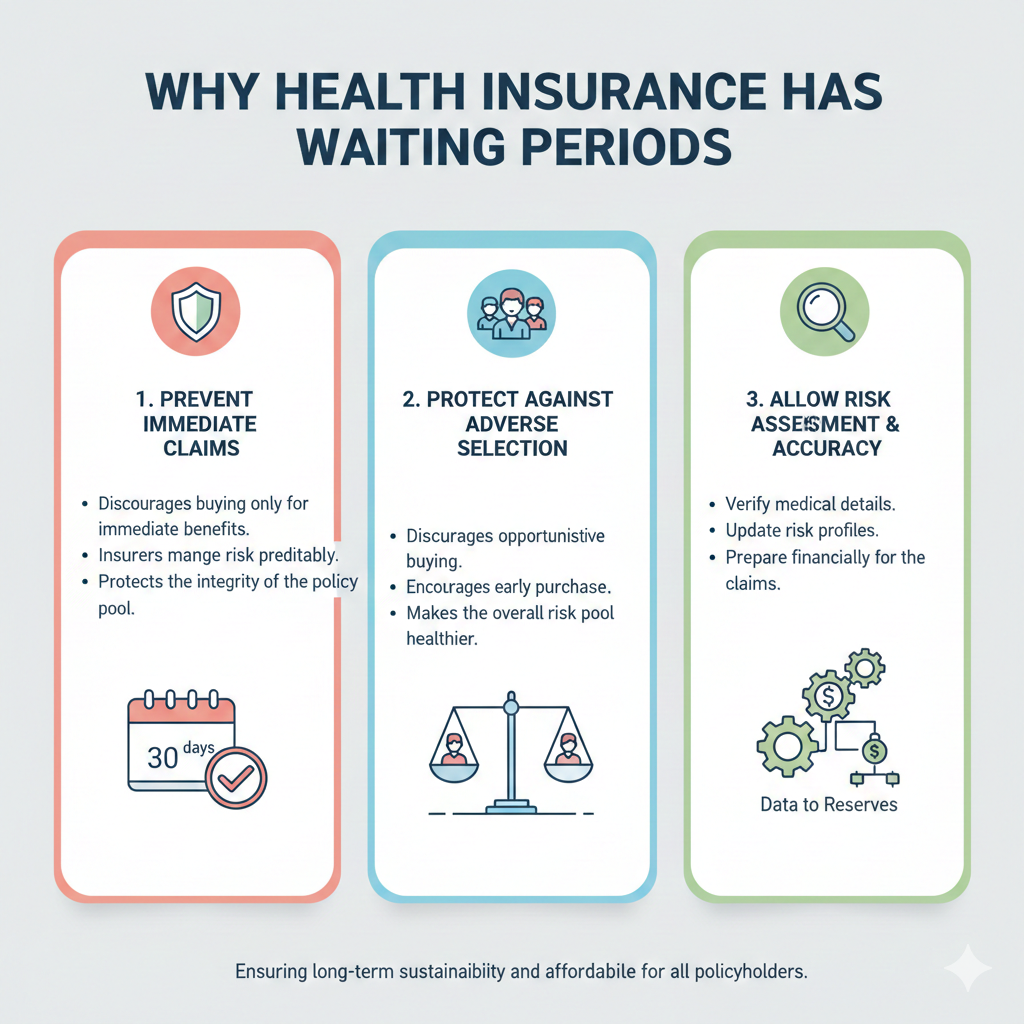

1. To Prevent Immediate Claims After Purchase

Imagine a scenario where someone buys a policy today, finds a health issue tomorrow, and immediately files a costly claim — that defeats the purpose of insurance.

Waiting periods discourage this kind of behavior by ensuring that:

- Policies are not purchased solely to claim immediate benefits

- Insurers can manage risk more predictably

This protects the integrity of the pool so all policyholders benefit in the long run.

2. To Protect Insurers Against Adverse Selection

Adverse selection happens when people with poor health or known medical issues buy insurance just before they need expensive treatment.

Waiting periods:

- Discourage opportunistic buying

- Encourage people to buy insurance earlier in life

- Make the overall risk pool healthier

When healthy and less healthy lives are mixed, the insurer can balance costs better and keep premiums affordable.

3. To Allow Risk Assessment and Pricing Accuracy

Health insurance companies don’t just collect premiums — they calculate risk, set appropriate premiums, and create financial reserves to meet future claims.

Waiting periods give insurers time to:

- Verify medical details accurately

- Update risk profiles for large policy portfolios

- Prepare financially for large claims

This contributes to the long-term sustainability of health plans.

Waiting Periods and Pre-Existing Diseases (What It Means)

The most confusing waiting period for many buyers is the Pre-Existing Disease (PED) waiting period. Let’s break down what that really means.

What Is a Pre-Existing Disease?

A pre-existing disease is any medical condition you had before the policy start date. Examples include:

- Diabetes

- Asthma

- Thyroid issues

- Hypertension

How PED Waiting Period Works

Most Indian health policies require you to wait a fixed period — commonly 2–4 years — before they will cover claims related to a pre-existing condition.

This waiting period:

- Doesn’t start over with renewals if policy is continuous

- Can often be reduced with a gapless transition when switching insurers

In insurance jargon, this is called policy portability — learn more about choosing plans and switching smartly here.

Why a 30-Day Waiting Period Exists on New Policies

Almost all health plans impose an initial waiting period (e.g., 30 days). This is meant to:

- Block immediate claims on minor ailments

- Cover only unexpected conditions after policy start date

However, many insurers waive the initial waiting period for accident-related treatments, because accidents are inherently unpredictable and not prone to adverse selection.

Economic Logic Behind Waiting Periods

Health insurance is all about risk pooling — collecting premiums from many to cover costs of the few who need treatment. This requires balance.

Here’s the economic logic that makes waiting periods vital:

🔹 They Reduce Moral Hazard

Moral hazard is when people act differently because they’re insured — for example:

Buying insurance only when they feel sick

Claiming for minor conditions immediately

Waiting periods curb this behavior.

🔹 They Keep Premiums Lower for Everyone

If people could claim immediately:

- Insurers would hike premiums dramatically

- Insurance would become unaffordable for many

In essence, waiting periods help keep premiums sustainable.

Do Waiting Periods Apply to All Treatments?

No — waiting periods vary by condition and policy. Some treatments may not have waiting periods if:

- They are emergency procedures

- They’re accident-related

- The policy specifically covers them early

Always read the policy wording carefully — that’s the legally binding part. (This will help.)

How to Reduce or Avoid Waiting Periods

There are a few strategies you can use to minimize the burden of waiting periods:

✳️ Policy Portability (Switching Insurers)

If you switch insurers without a break in coverage:

Waiting periods already served can be carried forward

This is regulated in India to protect consumers

✳️ Buy Early in Life

The younger and healthier you are:

- The fewer medical conditions you have

- The lower your risk profile becomes

- Waiting periods become less painful

✳️ Choose Policies with Shorter Waiting Periods

Some insurers offer reduced waiting periods as a differentiation strategy. Always compare!

Common Misconceptions About Waiting Periods

Let’s clear up some frequently misunderstood points.

❌ Myth: Waiting Periods Are Optional

No — they are contractual terms agreed upon when you buy the policy.

❌ Myth: You Can Get Around Them by Claiming Quickly

No — insurers will reject claims if they fall within waiting periods.

❌ Myth: Waiting Periods Apply Only to Major Illnesses

Waiting periods can apply to many conditions, including:

Pre-existing diseases

Certain surgeries

Specific ailments (like hernia)

Why Waiting Periods Matter for You (Policyholder Perspective)

Understanding waiting periods helps you:

✔ Avoid claim rejection surprises

✔ Plan healthcare spending ahead

✔ Choose the right policy at the right time

✔ Switch insurers without losing benefits

This boosts your overall financial security.

To better understand regulatory norms surrounding waiting periods, you can refer to the official IRDAI document here :- https://www.irdai.gov.in

This gives you insight into how insurance is governed in India.

—

Summary: Why Health Insurance Has Waiting Periods

Waiting periods exist because:

- They protect insurers from immediate claims

- They prevent adverse selection

- They keep premiums affordable and manageable

- They help maintain healthy risk pools

- They align with regulatory requirements

Rather than seeing waiting periods as obstacles, view them as mechanisms that make insurance sustainable for the long term.

—

❓ Frequently Asked Questions (FAQs)

1. Can I claim a health insurance benefit during the waiting period?

No — most claims during the waiting period are not covered unless they are specifically exempt (e.g., accidental injuries).

2. How long is the waiting period for pre-existing diseases in India?

Typically between 2 to 4 years, depending on the insurer and your medical history.

3. Does the waiting period restart when I renew my policy?

No — continuous renewals usually prevent resetting of already served waiting periods.

4. Can switching insurers help reduce waiting periods?

Yes — through policy portability, you can carry forward waiting periods served with your previous insurer.

5. Do waiting periods apply to all health insurance plans?

Almost all plans have waiting periods, but the duration and conditions vary from policy to policy.