At some point, almost everyone asks these questions — “Is health insurance a waste of money? or is it actually worth it? isn’t it just another expense draining my salary?”

When you’re young, relatively healthy, and already juggling EMIs, rent, and lifestyle costs, paying thousands every year for something you might never use can feel pointless. Many people even brag about never claiming their health insurance.

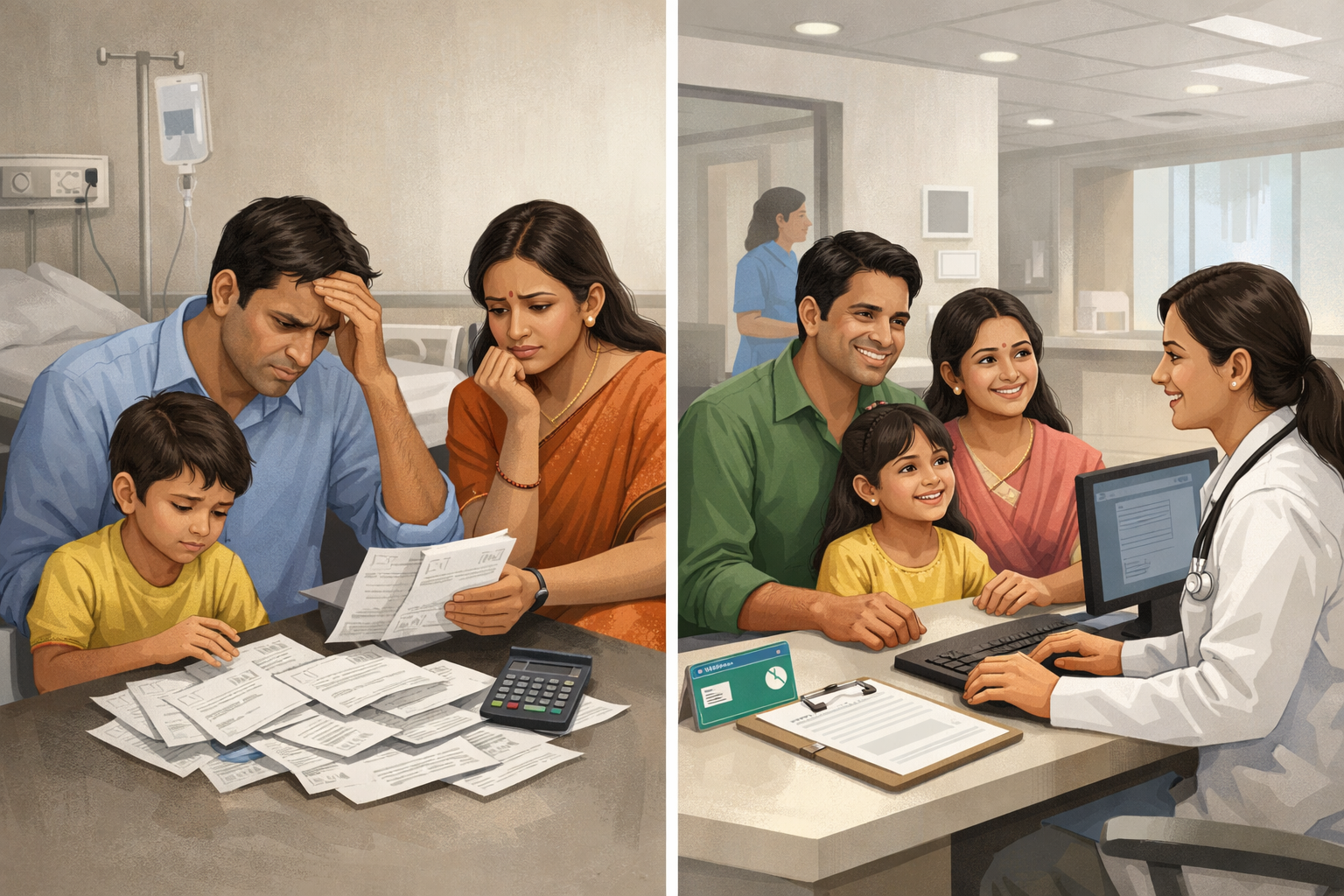

But here’s the uncomfortable truth: health insurance often feels like a waste of money right until the day it saves you financially.

In this article, we’ll break this down honestly — no fear-mongering, no sales pitch. You’ll understand when health insurance can feel like a waste, when it absolutely isn’t, and how to decide what makes sense for you.

Why People Think Health Insurance Is a Waste of Money

Let’s start with the mindset — because it’s not irrational.

1. “I’m Young and Healthy”

This is the most common reason. If you’re in your 20s or early 30s, rarely visit hospitals, and have no chronic conditions, insurance premiums can feel like money thrown into a black hole.

Many Indians go years without filing a single claim. Naturally, they begin to feel cheated.

2. Claims Feel Complicated and Uncertain

Stories of rejected claims, long hospital paperwork, and fine print don’t help. People worry:

- What if my claim gets rejected?

- What if the hospital isn’t covered?

This fear makes insurance feel unreliable.

3. Employer Health Insurance Creates False Comfort

A lot of people rely entirely on their company-provided health insurance. This creates the illusion that personal health insurance is unnecessary.

But employer cover:

- Ends when you switch jobs

- Often has low coverage limits

- May not cover parents adequately

We’ve covered this risk in detail in our guide on ‘how does health insurance work when I switch jobs?‘

4. “I’ll Pay Medical Bills If They Come”

Some believe self-funding medical costs is smarter. This works — until it doesn’t.

A single hospitalisation today can cost more than 10–15 years of premiums.

The Reality of Healthcare Costs in India

Healthcare inflation in India is among the highest globally, averaging 10–14% annually.

Here’s what that means in real life:

- A surgery costing ₹3 lakh today could cost ₹6–7 lakh in 6–7 years

- ICU stays can cross ₹10,000–₹15,000 per day

- Cancer treatments can easily run into ₹10–20 lakh

According to data shared by the IRDAI, medical expenses are one of the top reasons for financial distress among Indian households.

Saving alone struggles to keep up with this inflation — insurance pools this risk instead.

When Health Insurance Actually Feels Like a Waste

Let’s be fair — there are situations where health insurance may feel inefficient.

1. Very Low Coverage Policies

A ₹2–3 lakh cover sounds comforting but barely scratches the surface of modern medical costs. Such policies often:

- Get exhausted in one hospitalisation

- Give a false sense of security

This is why we recommend a minimum of ₹10–15 lakh for metro residents. You can read more in our detailed breakdown on ‘how much health insurance cover do you really need‘.

2. Buying the Wrong Policy

Choosing insurance based purely on:

- Lowest premium

- Brand name

- Agent pressure

can lead to exclusions, co-payments, and claim headaches later.

3. Short-Term Thinking

If you evaluate health insurance yearly like a mutual fund return, it will always disappoint. Insurance is protection, not profit.

When Health Insurance Is Absolutely Worth It

Now let’s flip the lens.

1. One Hospitalisation Can Undo Years of Savings

Even a middle-class family with decent savings can struggle if a major illness strikes.

Health insurance ensures:

- Your emergency fund stays intact

- Your investments aren’t liquidated at the worst time

- Your long-term goals stay protected

2. Cashless Treatment Reduces Stress

During a medical emergency, arranging money is the last thing you want to worry about.

Cashless hospitalisation allows you to focus on recovery instead of finances.

3. It Protects Your Family, Not Just You

Health insurance isn’t just about you. It prevents:

- Borrowing from relatives

- Dipping into children’s education funds

- Emotional stress during already difficult times

4. Becomes Priceless With Age

Premiums are lowest when you’re young. Waiting until health issues appear means:

- Higher premiums

- Waiting periods

- Possible rejection

Buying early is about insurability, not just savings.

Health Insurance vs Self-Funding: A Simple Comparison

| Aspect | Self-Funding | Health Insurance |

|---|---|---|

| Predictability | Low | High |

| Impact of large bills | Severe | Limited |

| Stress during emergencies | High | Lower |

| Inflation protection | Poor | Better |

Self-funding works best for small, routine expenses — not financial shocks.

How to Make Health Insurance Worth Every Rupee

Health insurance isn’t magic. You need to buy it right.

1. Choose Adequate Coverage

For most Indians:

- ₹10–15 lakh (individual)

- ₹20–30 lakh (family floater)

2. Prefer Personal Policy Over Employer Cover

Treat employer insurance as a bonus, not a base.

3. Look Beyond Premium

Focus on:

- Claim settlement ratio

- Hospital network

- No-claim bonus

- Room rent limits

Our comparison checklist on ‘how to determine which health insurance plan is best for you‘ can help.

4. Don’t Skip Reading the Policy

Boring? Yes. Necessary? Absolutely.

So, Is Health Insurance a Waste of Money?

Short answer: No — but it can feel like one if you buy it blindly or expect returns.

Health insurance is not an investment. It’s a financial seatbelt. You hope you never need it — but if you do, you’ll be glad it’s there.

The real waste of money is:

- Underinsuring yourself

- Relying only on employer cover

- Assuming “nothing will happen”

Because healthcare emergencies don’t ask for permission — and they don’t come cheap. (our this article can help you too.)

If you’re building long-term financial security, health insurance isn’t optional — it’s foundational.

Frequently Asked Questions (FAQs)

1. Is health insurance worth it for young people in India?

Yes. Buying early locks in lower premiums and ensures coverage before health issues appear.

2. Can I rely only on employer-provided health insurance?

No. Employer insurance is temporary and often insufficient for major medical costs.

3. What happens if I never use my health insurance?

Then it did its job — you stayed protected. Insurance is about risk transfer, not usage.

4. How much health insurance cover is enough?

For most individuals, at least ₹10–15 lakh is recommended, depending on city and lifestyle.

5. Is health insurance better than saving money for medical emergencies?

Yes. Savings alone struggle against medical inflation and large, unexpected expenses.