Healthcare costs in India are rising quietly but steadily. Even for central government employees and pensioners covered under CGHS, a single hospitalisation can sometimes lead to unexpected expenses, delayed reimbursements, or partial coverage. This is exactly the gap Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries is trying to fill.

Instead of replacing CGHS, this scheme works alongside it — offering an extra layer of financial protection when medical bills go beyond comfort. In this article, we’ll break down Paripoorna Mediclaim Ayush Bima in plain language, without legal jargon or promotional fluff, so you can decide whether it actually makes sense for you or your family.

Why Paripoorna Mediclaim Ayush Bima Was Introduced

CGHS is a strong foundation for healthcare, but it isn’t perfect. Many beneficiaries have faced situations where:

- Hospital package rates exceed CGHS limits

- Certain treatments are only partially reimbursed

- Advanced procedures involve out-of-pocket payments

- Pensioners feel financially exposed during major illnesses

Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries was introduced to address these exact pain points. It acts as a financial buffer, stepping in when CGHS alone doesn’t fully cover hospitalisation costs.

What Is Paripoorna Mediclaim Ayush Bima?

In simple terms, Paripoorna Mediclaim Ayush Bima is an optional health insurance policy designed exclusively for CGHS beneficiaries. It provides additional hospitalisation coverage, including AYUSH treatments, modern medical procedures, and cashless care at empanelled hospitals.

A few things to be very clear about:

- It is not free

- It is not compulsory

- It does not replace CGHS

Think of it as a backup plan — one that protects your savings when medical expenses rise unexpectedly.

Who Can Buy Paripoorna Mediclaim Ayush Bima?

This policy is available only to:

- Serving central government employees enrolled under CGHS

- Retired central government employees (CGHS pensioners)

- Eligible dependent family members

A single policy can usually cover up to six family members, making it practical for most households. If you are not a CGHS beneficiary, this scheme is not applicable.

Coverage Options Under Paripoorna Mediclaim Ayush Bima

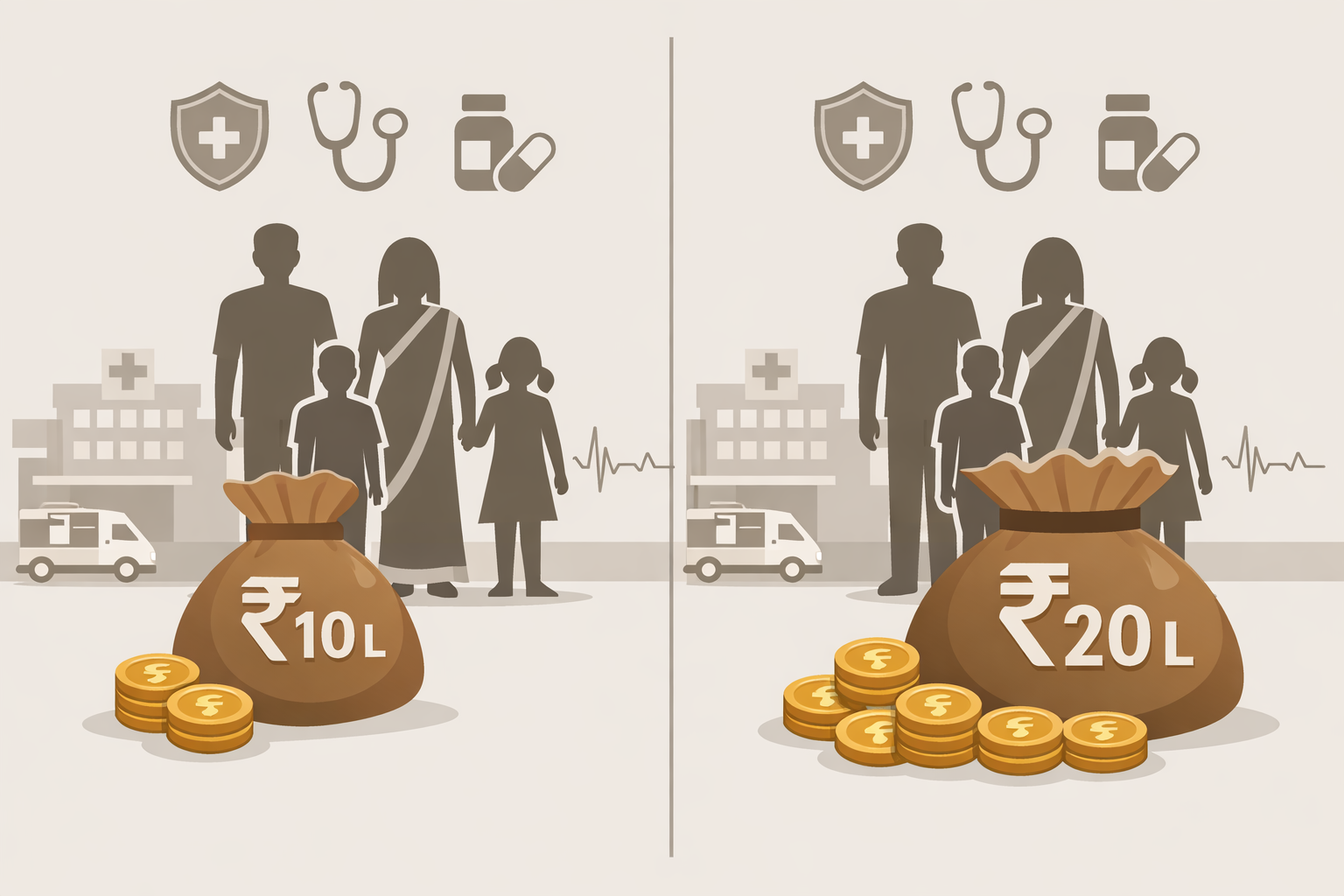

Under Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries, you can choose between two sum insured options:

- ₹10 lakh

- ₹20 lakh

This coverage applies to in-patient hospitalisation within India. For many CGHS families, this amount can significantly reduce financial stress during major medical events.

Understanding the Co‑Payment Structure

One unique aspect of Paripoorna Mediclaim Ayush Bima is the co-payment option. This means you agree to share a portion of the hospital bill with the insurer.

You can choose:

- 70:30 co-payment – Insurer pays 70%, you pay 30%

- 50:50 co-payment – Insurer pays 50%, you pay 50%

Why would anyone choose this?

Because co-payment significantly reduces the premium. For many pensioners and senior beneficiaries, this makes the policy far more affordable while still offering meaningful protection.

Hospitalisation Benefits:

Cashless Treatment

Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries offers cashless hospitalisation at empanelled hospitals. This reduces the hassle of paying large sums upfront and waiting for reimbursements.

Room Rent Limits

To keep costs under control:

- Normal room: up to 1% of sum insured per day

- ICU: up to 2% of sum insured per day

These limits help prevent inflated hospital bills.

Pre and Post Hospitalisation Coverage

Medical expenses related to hospitalisation are covered:

- 30 days before admission

- 60 days after discharge

This includes diagnostic tests, medicines, and follow‑up consultations.

AYUSH Coverage: A Major Strength

One of the standout features of Paripoorna Mediclaim Ayush Bima is its strong focus on AYUSH treatments. In-patient treatments under:

- Ayurveda

- Yoga & Naturopathy

- Unani

- Siddha

- Homeopathy

are covered up to 100% of the sum insured, provided hospital admission is required.

For beneficiaries who trust traditional Indian systems of medicine, this makes Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries especially valuable.

Coverage for Modern Medical Treatments

Modern and advanced treatments are covered up to 25% of the sum insured by default. There is also an optional rider available to increase this coverage further, subject to policy terms.

This ensures the policy remains relevant even for advanced procedures and evolving medical technologies.

Cumulative Bonus for Claim‑Free Years

Staying healthy comes with rewards.

Under Paripoorna Mediclaim Ayush Bima, you earn:

- 10% cumulative bonus for every claim‑free year

- Bonus accumulation up to 100% of base sum insured

Over time, this can effectively double your coverage without increasing your premium.

No GST on Premium

Unlike most private health insurance policies, Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries does not attract GST. This keeps premiums lower and improves long‑term affordability.

How This Policy Works with CGHS

It’s important to understand that Paripoorna Mediclaim Ayush Bima does not replace CGHS. CGHS remains your primary healthcare system for OPD services, consultations, and routine care.

This policy steps in when:

- Hospital costs exceed CGHS package limits

- Reimbursements are delayed or partial

- Advanced or specialised treatments are needed

Together, CGHS and Paripoorna Mediclaim Ayush Bima create a stronger safety net.

A Practical Example

Consider a CGHS pensioner who undergoes a surgery costing ₹12 lakh:

- CGHS covers part of the expense

- The remaining amount is claimed under Paripoorna Mediclaim Ayush Bima

- Co‑payment keeps personal expenses predictable

- Cashless treatment avoids reimbursement stress

- Pre and post‑hospitalisation expenses are also covered

This is where Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries truly shows its value.

Is Paripoorna Mediclaim Ayush Bima Worth Considering?

This policy may be a good fit if:

- You are a CGHS beneficiary concerned about rising medical costs

- You want extra protection during major hospitalisation

- You prefer predictable healthcare expenses

- You value AYUSH and holistic treatment options

- You want insurance without GST and with long‑term bonuses

It may not be necessary for everyone, but for many families — especially pensioners — it fills a genuine gap.

External References (Recommended Reading)

To help you understand the broader context and make informed decisions, here are some useful external resources related to Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries.

For official confirmation and deeper understanding, the following authoritative sources provide reliable information related to Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries:

- Official announcements and clarifications published by the Press Information Bureau (PIB), Government of India: https://pib.gov.in

- Policy updates and notifications issued by the Department of Financial Services, Ministry of Finance: https://financialservices.gov.in

- CGHS-related circulars and beneficiary guidelines available on the Central Government Health Scheme (CGHS) portal: https://cghs.gov.in

- Product-level details and enrolment updates expected from New India Assurance Company Limited, the implementing public sector insurer: https://www.newindia.co.in

These external links help verify scheme details, government intent, and insurer-level implementation while improving transparency and reader trust.

Final Thoughts

Paripoorna Mediclaim Ayush Bima for CGHS beneficiaries is not a flashy product, but it is a practical one. It quietly strengthens financial security, reduces uncertainty, and complements CGHS in areas where real‑world medical expenses often exceed expectations.

If CGHS is your foundation, Paripoorna Mediclaim Ayush Bima acts as the safety net — and for many households, that peace of mind is worth a lot.

Frequently Asked Questions (FAQs)

1. What is Paripoorna Mediclaim Ayush Bima?

Paripoorna Mediclaim Ayush Bima is an optional health insurance policy designed specifically for CGHS beneficiaries. It provides additional hospitalisation coverage, including AYUSH and modern treatments, on top of existing CGHS benefits.

2. Is Paripoorna Mediclaim Ayush Bima free for CGHS beneficiaries?

No. Paripoorna Mediclaim Ayush Bima is not free. Beneficiaries need to pay a premium to purchase the policy. However, premiums are lower due to co‑payment options and the absence of GST.

3. Who is eligible for Paripoorna Mediclaim Ayush Bima?

Only CGHS beneficiaries — including serving central government employees, CGHS pensioners, and their eligible dependent family members — can buy this policy.

4. Does Paripoorna Mediclaim Ayush Bima replace CGHS?

No. This policy does not replace CGHS. It works alongside CGHS to cover hospitalisation expenses that exceed CGHS package limits or are not fully reimbursed.

5. Are AYUSH treatments covered under Paripoorna Mediclaim Ayush Bima?

Yes. In‑patient AYUSH treatments such as Ayurveda, Yoga & Naturopathy, Unani, Siddha, and Homeopathy are covered up to 100% of the sum insured, subject to policy conditions.