How to Buy Health Insurance in India: A Step-by-Step Guide for First-Time Buyers

Health insurance has become a critical part of personal financial planning in India. With rising medical inflation, increasing lifestyle-related diseases, and the high cost of private healthcare, a single hospitalization can significantly strain your savings. Yet, despite its importance, many people delay buying health insurance or make poor choices due to confusion and misinformation.

Step by step, using a practical, regulator-backed approach, this guide answers your question- how to buy health insurance in India? Whether you are a first-time buyer or reassessing an existing policy, this article will help you make an informed and confident decision.

Why Buying Health Insurance Is Important?

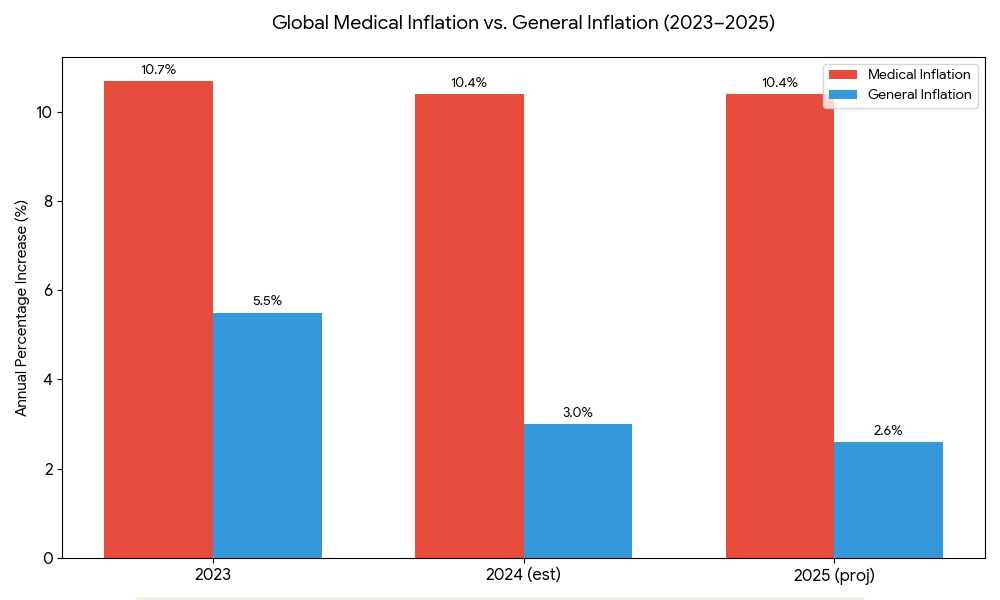

Healthcare costs in India have consistently risen over the last decade. According to data referenced by the World Health Organization (WHO), medical inflation globally outpaces general inflation, making healthcare unaffordable without financial protection.

In India, most quality healthcare is provided by private hospitals, where treatment costs are largely out-of-pocket. Health insurance acts as a financial safety net, protecting your savings and ensuring access to timely medical care during emergencies.

Step 1: Understand Your Healthcare Needs

Before comparing insurance plans, start by evaluating your personal and family healthcare requirements.

Key Questions to Ask Yourself

- Are you buying insurance for yourself, your family, or senior parents?

- Do you have any pre-existing medical conditions?

- Do you live in a metro city or a smaller town?

- How frequently do you or your family require medical care?

Your age, lifestyle, family size, and medical history directly influence the type of policy you should choose.

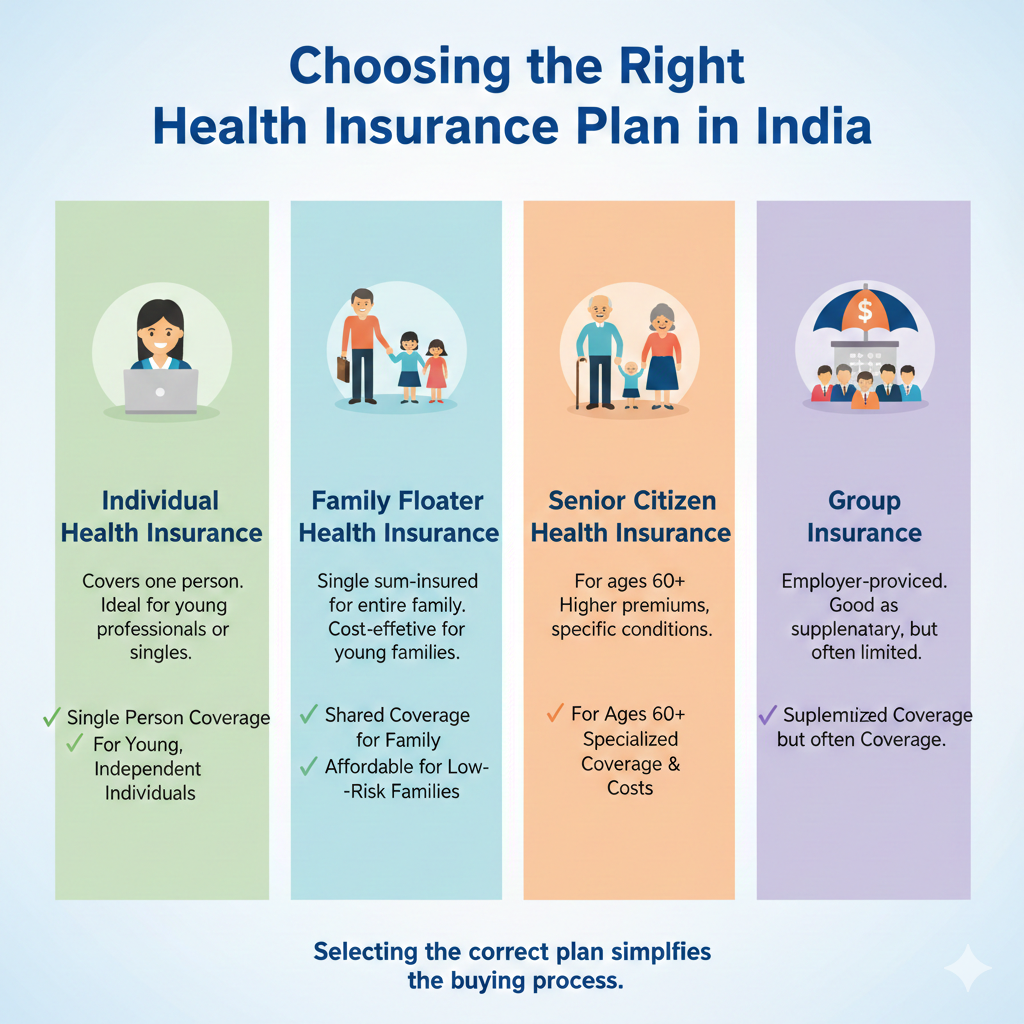

Step 2: Choose the Right Type of Health Insurance Plan

Health insurance policies in India are broadly categorized into different types. Selecting the correct one simplifies the buying process.

Individual Health Insurance

Covers one person under a single policy. Suitable for young professionals or individuals without dependents.

Family Floater Health Insurance

A single sum insured shared among family members. Cost-effective for young families with low medical risk.

Senior Citizen Health Insurance

Designed for individuals aged 60 and above. These plans usually have higher premiums and specific coverage conditions.

Group Health Insurance

Provided by employers. Useful as supplementary coverage but often insufficient on its own.

Step 3: Decide the Right Sum Insured

Choosing the correct sum insured is crucial. Underinsuring can lead to high out-of-pocket expenses during hospitalization.

Factors That Affect the Required Coverage

- City of residence and hospital costs

- Age and health condition of insured members

- Family size

- Rising medical inflation (Medical inflation and healthcare financing are closely linked to India’s broader financial system, overseen by the Reserve Bank of India (RBI))

For many urban households in India, a ₹10–15 lakh sum insured is increasingly considered a practical starting point.

Step 4: Understand What the Policy Covers

A good health insurance policy should provide comprehensive coverage beyond basic hospitalization.

Important Coverage Features to Look For

- In-patient hospitalization

- Pre- and post-hospitalization expenses

- Daycare procedures

- Ambulance charges

- Organ donor expenses

- Mental health treatment (mandated by IRDAI)

- AYUSH treatments (if relevant)

Understanding inclusions helps avoid unpleasant surprises during claims.

Step 5: Be Honest About Pre-Existing Diseases

One of the most common mistakes buyers make is hiding pre-existing conditions to get a lower premium.

Why Full Disclosure Is Essential

- Non-disclosure can lead to claim rejection

- Policies are issued based on risk assessment

- Waiting periods apply regardless of insurer

Pre-existing diseases usually have a waiting period of 2–4 years, which is standard and regulated by IRDAI.

Step 6: Understand Waiting Periods and Exclusions

Waiting periods and exclusions are part of every health insurance policy.

Common Types of Waiting Periods

- Initial waiting period (usually 30 days)

- Pre-existing disease waiting period

- Disease-specific waiting periods

Reading the policy wording carefully helps you understand when coverage actually begins.

Step 7: Evaluate the Claim Settlement Process

The real value of health insurance lies in how smoothly claims are settled.

What to Look Beyond Claim Settlement Ratio

- Cashless claim approval speed

- In-house claim processing vs TPA

- Customer grievance redressal system

IRDAI publishes claim-related data that helps assess insurer credibility objectively.

Step 8: Check Network Hospitals and Cashless Facilities

Network hospitals enable cashless treatment, reducing financial stress during emergencies.

Why Network Coverage Matters

- Access to nearby hospitals

- Faster claim processing

- Reduced upfront payments

Always verify whether hospitals near your residence are included in the insurer’s network.

Step 9: Compare Premiums Wisely

Premium affordability is important, but it should not be the sole deciding factor.

Risks of Choosing Extremely Cheap Plans

- High co-payment clauses

- Room rent sub-limits

- Disease-specific caps

- Longer waiting periods

Focus on value for money, not just the lowest premium. Understanding how insurers price policies becomes easier once you know how health insurance companies make money, including risk pooling, claims ratios, and investment income

Step 10: Check Co-Payment, Deductibles, and Sub-Limits

Cost-sharing clauses directly affect your out-of-pocket expenses.

Key Terms to Understand

- Co-payment percentage

- Disease-specific sub-limits

- Deductible amounts

Policies with fewer restrictions offer better predictability during claims.

Step 11: Ensure Lifelong Renewability

Health insurance provides maximum benefit when maintained continuously.

Why Lifelong Coverage Is Important

- Waiting periods need not be served again

- Coverage continues into old age

- Protection against age-related exclusions

IRDAI mandates lifelong renewability for most retail health insurance policies.

Step 12: Use Riders and Add-ons Carefully

Add-ons can enhance coverage but should be chosen selectively.

Useful Add-ons to Consider

- Restoration of sum insured

- Room rent waiver

- No-claim bonus protection

Avoid unnecessary riders that inflate premiums without real benefits.

Step 13: Read the Policy Document Thoroughly

The policy wording is the legally binding document—not marketing brochures.

What to Check in Policy Wording

- Definitions of medical terms

- Exclusions and limitations

- Claim documentation requirements

- Renewal conditions

Clarity at the time of purchase prevents disputes later.

Final Thoughts: Buying Health Insurance the Right Way

Buying health insurance is not about choosing the cheapest or most popular plan. The right policy balances coverage, affordability, and usability while aligning with your long-term healthcare needs.

Understanding how health insurance companies make money and how policies are structured helps you evaluate premiums, exclusions, and claim limits more objectively. Health insurance works best as a long-term financial safety net, not a short-term transaction.

FAQs: How to Buy Health Insurance in India

1. Is health insurance mandatory in India?

No, health insurance is not legally mandatory, but it is strongly recommended due to rising healthcare costs.

2. Is employer-provided health insurance enough?

Employer policies offer basic coverage but often have low limits and end when you leave the job. A personal policy ensures continuity.

3. How early should I buy health insurance?

Buying health insurance at a younger age reduces premiums, medical checks, and waiting periods.

4. Can I switch my health insurance policy later?

Yes. Portability allows you to switch insurers while retaining waiting period benefits, subject to conditions.

5. Should I buy health insurance online or offline?

Both options are valid. What matters most is understanding the policy terms and coverage details.