When my wife and I started planning a family, health insurance wasn’t top of mind. We were thinking about names, nursery colors, and whether we were ready for parenthood. That changed when a friend shared her hospital bill—₹2.8 lakhs for a normal delivery.

That moment made one thing clear: health insurance with maternity cover isn’t optional anymore—it’s planning.

If you’re thinking about having a baby in the next few years, this guide will help you understand how maternity insurance works in India, what to look for, and how to avoid expensive mistakes.

Why Health Insurance with Maternity Cover Matters

Childbirth costs in India have risen sharply, especially in private hospitals, as highlighted in maternal healthcare data from the Ministry of Health & Family Welfare.

- Normal delivery: ₹50,000 to ₹1.5 lakh

- C-section: ₹1 lakh to ₹3 lakh or more

These figures don’t include:

- Prenatal checkups

- Ultrasounds and tests

- Postnatal care

- Newborn complications or NICU stays

Most employer-provided policies either exclude maternity or cap it tightly. That’s why personal health insurance with maternity cover is critical if you want choice, quality care, and financial peace of mind.

More couples are realizing this early—and planning ahead is the only way maternity insurance actually works.

(learn more about rising cost of hospitalisation for childbirth in India in this article.)

The Waiting Period Reality (This Is Non-Negotiable)

Maternity benefits come with waiting periods. There’s no workaround.

- Comprehensive health insurance: 2–4 years

- Maternity riders or add-ons: 9–12 months

You cannot buy health insurance with maternity cover after you’re already pregnant and expect it to pay for that pregnancy.

This is why timing matters more than price. If there’s even a chance you’ll start a family in the next few years, the clock needs to start now.

(Read more about maternity waiting period in our this article.)

Types of Health Insurance with Maternity Cover

1. Standalone Maternity Health Insurance

These plans focus almost entirely on pregnancy and childbirth.

Pros

- Short waiting period (9–12 months)

- Defined maternity benefits

- Newborn coverage for early months

Cons

- Higher premiums

- Limited coverage beyond maternity

Best if pregnancy is planned soon and you already have basic health insurance.

2. Comprehensive Health Insurance with Maternity Rider

This is the most common and practical option.

What it offers

- Full medical coverage + maternity benefits

- Family floater options

- Better long-term value

Trade-off

- Longer waiting period (usually 2–3 years)

For most couples, this is the smartest way to buy health insurance with maternity cover.

3. Employer or Group Health Insurance

Some corporate plans include maternity benefits with no waiting period.

Use it—but don’t depend on it. Job changes, insurer switches, or policy downgrades can remove maternity cover overnight. A personal policy is your safety net.

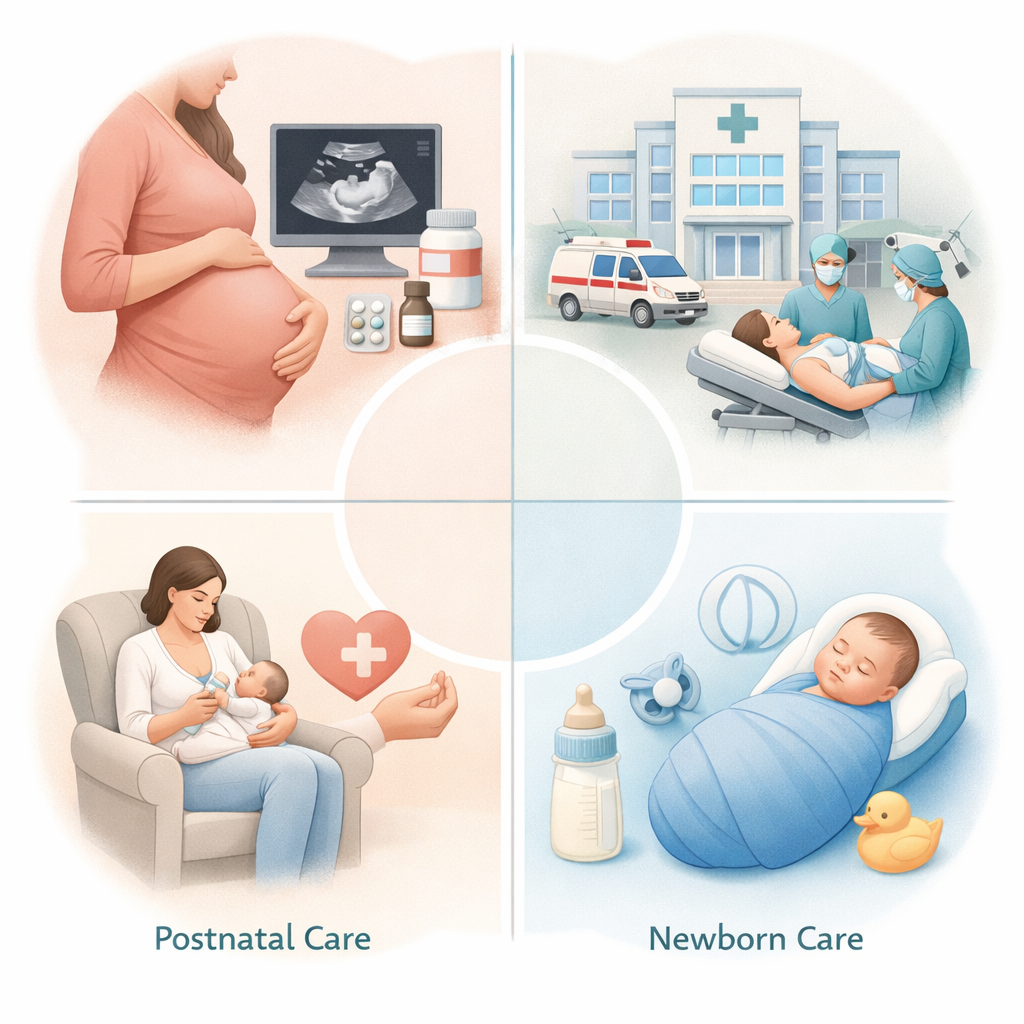

What Health Insurance with Maternity Cover Usually Includes

Prenatal Care

- Doctor consultations

- Blood tests and scans

- Pregnancy-related diagnostics

- Medications

Delivery Expenses

- Normal delivery

- C-section (usually higher limits)

- Hospital room charges

- Doctor, surgeon, and anesthesia fees

Postnatal Care

- Follow-ups after delivery

- Complications related to childbirth

- Recovery period (30–90 days)

Newborn Coverage

- Birth complications

- NICU expenses (if covered)

- Vaccinations

- Healthcare for the first 30–90 days

Common Exclusions

- IVF and fertility treatments

- Surrogacy

- Non-medical abortions

- Cosmetic procedures

Always confirm exclusions in the policy wording.

How to Choose the Right Health Insurance with Maternity Cover

Step 1: Estimate Real Hospital Costs

Call hospitals in your city and ask about delivery packages. This gives you a realistic baseline.

General guidance

- ₹3–5 lakh: basic private hospital coverage

- ₹7–10 lakh: metro cities, private rooms, complications

Step 2: Match the Waiting Period to Your Timeline

- Planning within 1–1.5 years → 9–12 month waiting period plans

- Planning later → comprehensive plans with longer waits but better coverage

Also check waiting periods for pregnancy-related complications.

Step 3: Watch for Sub-Limits (This Is Critical)

A ₹5 lakh policy is meaningless if:

- Normal delivery is capped at ₹75,000

- Room rent is limited to ₹5,000/day

Key sub-limits to review:

- Room rent

- Normal vs C-section delivery

- Prenatal and postnatal expenses

- Newborn care

Prefer plans with no sub-limits or high caps.

(if you want to insure your unborn baby’s health, this article might help.)

Step 4: Confirm Network Hospitals

Cashless delivery matters. Make sure:

- Your preferred hospital is in-network

- The insurer supports maternity cashless claims there

Step 5: Check Claim Settlement Reputation

Look beyond ads.

- Claim settlement ratio (90%+ is ideal)

- Real maternity claim experiences

- Ease of cashless approvals

Maternity claims can be stricter than regular hospital claims.

(Check the insurer’s claim settlement ratio published by the Insurance Regulatory and Development Authority of India (IRDAI) before buying a policy.)

Popular Health Insurance Plans with Maternity Cover

(Some coverage details vary by plan variant.)

- Star Health Comprehensive

- HDFC Ergo Health Suraksha

- Care Health Insurance

- ICICI Lombard Health Advantage

- Niva Bupa ReAssure

Always read the policy document—aggregator summaries miss fine print.

Cost of Health Insurance with Maternity Cover (Realistic Numbers)

Individual policy (woman, 28–30 years)

- ₹5 lakh cover: ₹10,000–₹18,000/year

- ₹10 lakh cover: ₹18,000–₹28,000/year

Family floater (couple)

- ₹5 lakh cover: ₹15,000–₹25,000/year

- ₹10 lakh cover: ₹25,000–₹40,000/year

Maternity benefits typically increase premiums by 20–40%, but one delivery can recover several years of premiums.

Practical Tips That Actually Help

- Buy early: Lower premiums, fewer eligibility issues

- Prefer family floaters if married or marrying soon

- Choose longer newborn coverage (90 days is better than 30)

- Ensure day-care procedures are covered

- Keep documents ready: marriage certificate, medical records, policy copy

Mistakes to Avoid

- Waiting until pregnancy

- Ignoring sub-limits

- Choosing based only on premium

- Assuming employer cover is permanent

- Forgetting Section 80D tax benefits

If You’re Already Pregnant

You can’t add maternity cover for the current pregnancy. Your options are:

- Employer insurance

- Hospital payment plans

- Government maternity schemes

- Buying insurance now for future pregnancies

The Bottom Line

Health insurance with maternity cover is about control and calm—not just cost savings.

When the time comes, you want:

- The hospital you trust

- The doctor you choose

- Zero stress about bills

If parenthood is even a remote possibility in the next few years, start your waiting period now. It’s one of those decisions your future self will quietly thank you for.

FAQs (Short & Crisp)

1. What is the waiting period for health insurance with maternity cover?

Usually 2–4 years for comprehensive plans and 9–12 months for maternity riders.

2. Can I buy maternity insurance after getting pregnant?

No. Coverage must start before conception and after completing the waiting period.

3. Does maternity insurance cover C-sections?

Yes, but often with higher sub-limits than normal delivery. Always check caps.

4. How much maternity cover should I take?

₹5–7 lakh minimum; ₹10 lakh if you want flexibility in metro cities.

5. Are prenatal and postnatal expenses covered?

Yes, but usually with specific limits. Check policy caps carefully.