Pregnancy is exciting—but it also brings a quiet fear that most parents don’t talk about openly: what if something goes wrong medically, and how will we afford it?

Over the past few years, a term has started appearing in hospital counselling rooms and insurance brochures—fetal health insurance. Some call it unborn baby insurance, others see it as a niche add-on. Many parents aren’t sure whether it’s genuinely useful or just another complicated insurance product.

This guide explains fetal health insurance in India in plain language—what it is, how it works, why it exists, and whether it actually makes sense for Indian families.

What Is Fetal Health Insurance in India?

Fetal health insurance in India is a health insurance cover that protects an unborn baby against congenital and birth-related medical conditions, starting during pregnancy and continuing after birth.

It usually becomes active after a certain gestational period and is offered as:

- An add-on rider to the mother’s health insurance, or

- A feature within select maternity or family floater plans

Once the baby is born, the coverage typically continues without fresh waiting periods.

Fetal health insurance in India covers congenital disorders and neonatal complications diagnosed during pregnancy, providing financial protection for the unborn child before and after birth.

Why Fetal Health Insurance in India Exists at All

For decades, health insurance in India followed a simple rule:

Insurance starts after birth.

That created a major gap.

The problem parents faced

- Congenital conditions were excluded for years due to waiting periods

- Neonatal ICU costs were not covered

- Parents paid lakhs out of pocket during the most vulnerable time

What changed?

Fetal health insurance in India emerged to fix this exact gap, driven by four big shifts:

- Advanced prenatal testing detecting abnormalities early

- Skyrocketing NICU costs in private hospitals

- Post-COVID insurance awareness

- Regulatory flexibility from IRDAI

In short, medicine moved faster than insurance—and fetal cover is insurance catching up.

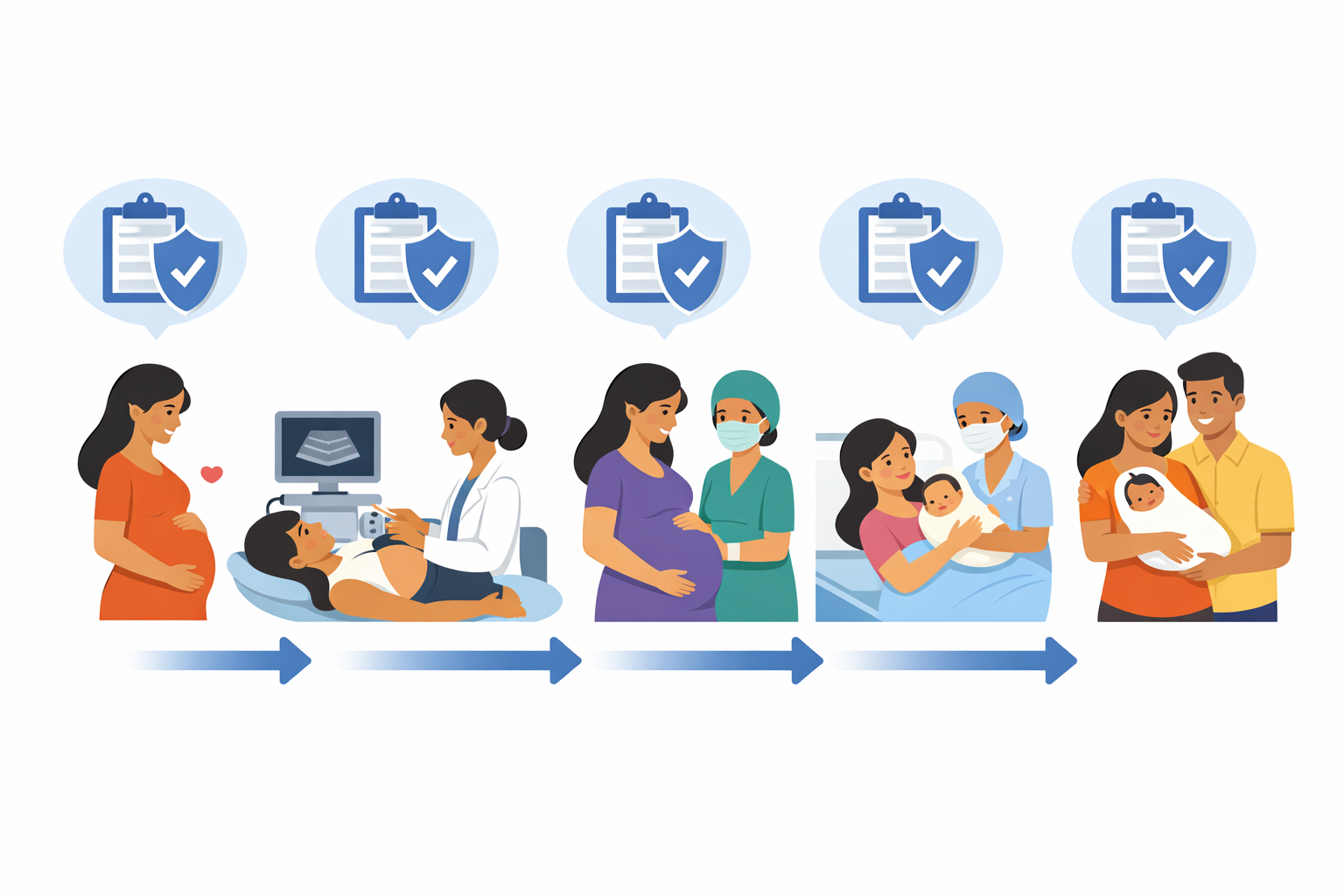

How Fetal Health Insurance in India Works (Step by Step)

Step 1: Policy Is Purchased During Pregnancy

Fetal health insurance in India must be bought:

- After a minimum gestational age (often 12–20 weeks)

- Before any fetal abnormality is detected

Once a condition is already diagnosed, insurers usually exclude or reject coverage.

Step 2: The Unborn Baby Gets Covered

From activation:

- The fetus is insured as a dependent

- Congenital and birth-related conditions are eligible

This is the most important distinction from regular insurance.

Step 3: Coverage Continues After Birth

After delivery:

- The baby remains insured automatically

- No new waiting periods apply for covered conditions

This continuity is what makes fetal health insurance in India valuable.

What Does Fetal Health Insurance in India Cover?

Coverage differs slightly across insurers, but most plans include:

1. Congenital Disorders

- Congenital heart defects

- Neural tube defects

- Genetic or metabolic conditions

2. Birth-Related Complications

- Premature birth issues

- Low birth weight complications

- Respiratory distress

3. Neonatal ICU (NICU) Expenses

- ICU stay

- Ventilator support

- Emergency neonatal surgeries

4. Treatment Linked to Prenatal Diagnosis

If a condition is identified during pregnancy and treated after birth, expenses may be covered.

What Fetal Health Insurance in India Usually Does NOT Cover

This is where confusion often arises.

Fetal health insurance in India typically does not cover:

- Normal delivery expenses

- Routine maternity costs

- Conditions detected before buying the policy

- Non-medical or cosmetic procedures

Maternity insurance and fetal insurance serve different purposes—they are not interchangeable.

Is Fetal Health Insurance in India the Same as Maternity Insurance?

No—and mixing them up is a common mistake.

| Feature | Maternity Insurance | Fetal Health Insurance in India |

|---|---|---|

| Covers delivery costs | Yes | Usually no |

| Covers unborn baby | No | Yes |

| Covers congenital diseases | Rarely | Yes |

| Waiting period | 2–4 years | Often waived |

| When to buy | Before pregnancy | During pregnancy |

Ideally, fetal health insurance in India acts as a risk shield, not a routine expense cover.

Is Fetal Health Insurance in India a New Concept?

Short answer:

- Globally: Not new

- In India: Relatively new and still evolving

Until about 2020–2022, insurers rarely offered formal fetal cover. Most child policies started only after birth, with exclusions that made congenital coverage almost useless early on.

Fetal health insurance in India is still:

- Not standardised

- Mostly offered as riders

- Poorly understood—even by some agents

Who Should Consider Fetal Health Insurance in India?

You may want to seriously consider fetal health insurance in India if:

- You’re delivering in a private hospital

- There’s a family history of congenital disorders

- The pregnancy involves advanced maternal age

- You want protection from high-cost, low-probability risks

It may be less useful if:

- You rely entirely on government hospitals

- Your employer already offers strong dependent coverage

A Simple Real-Life Scenario

An anomaly scan at 24 weeks detects a congenital heart condition. Surgery after birth costs ₹7–10 lakh.

- Without fetal health insurance in India: Parents self-fund treatment

- With fetal health insurance in India: NICU and surgery may be covered

This is why the product exists—not for routine cases, but for rare, high-impact ones.

Key Things to Check Before Buying Fetal Health Insurance in India

Before signing anything, verify:

- Minimum and maximum gestational age

- List of covered congenital conditions

- NICU sub-limits

- Continuity clause after birth

- Clear exclusions in policy wording

For regulatory clarity, refer directly to:

- IRDAI – https://www.irdai.gov.in

- National Health Portal – https://www.nhp.gov.in

- NHS congenital condition resources – https://www.nhs.uk

Is Fetal Health Insurance in India Worth It?

There’s no universal yes or no.

Fetal health insurance in India is not mandatory or essential for everyone.

But for parents who want financial certainty during medical uncertainty, it can be a rational decision—not an emotional one.

Think of it as catastrophic risk protection, not routine insurance.

Final Takeaway

Fetal health insurance in India fills a gap that traditional health insurance ignored for decades. While the product is still evolving and imperfect, it reflects a real shift in how pregnancy-related risks are being handled.

If you’re expecting, informed, and planning ahead, understanding fetal health insurance puts you in control—rather than leaving you vulnerable during one of life’s most delicate moments.

Frequently Asked Questions (FAQs)

1. Is fetal health insurance in India approved by IRDAI?

Yes. It is allowed, usually as a rider or add-on under existing health policies.

2. When should fetal health insurance in India be purchased?

Ideally between 12 and 20 weeks of pregnancy, before any abnormality is detected.

3. Does fetal health insurance in India cover delivery costs?

No. Delivery expenses are covered only under maternity insurance.

4. Is fetal health insurance in India compulsory?

No. It is completely optional.

5. Does coverage continue after the baby is born?

Yes, most policies allow seamless continuation without waiting periods.