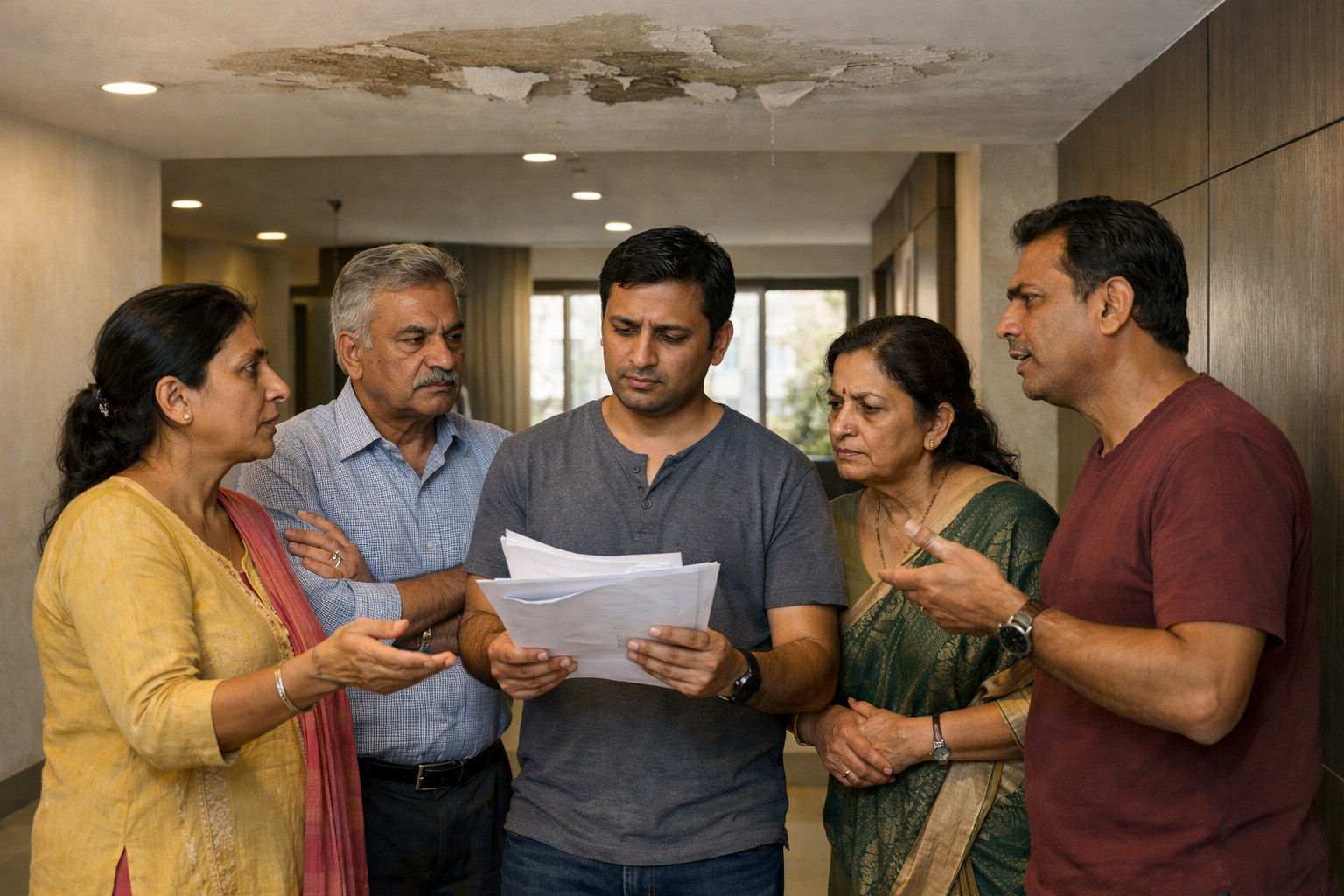

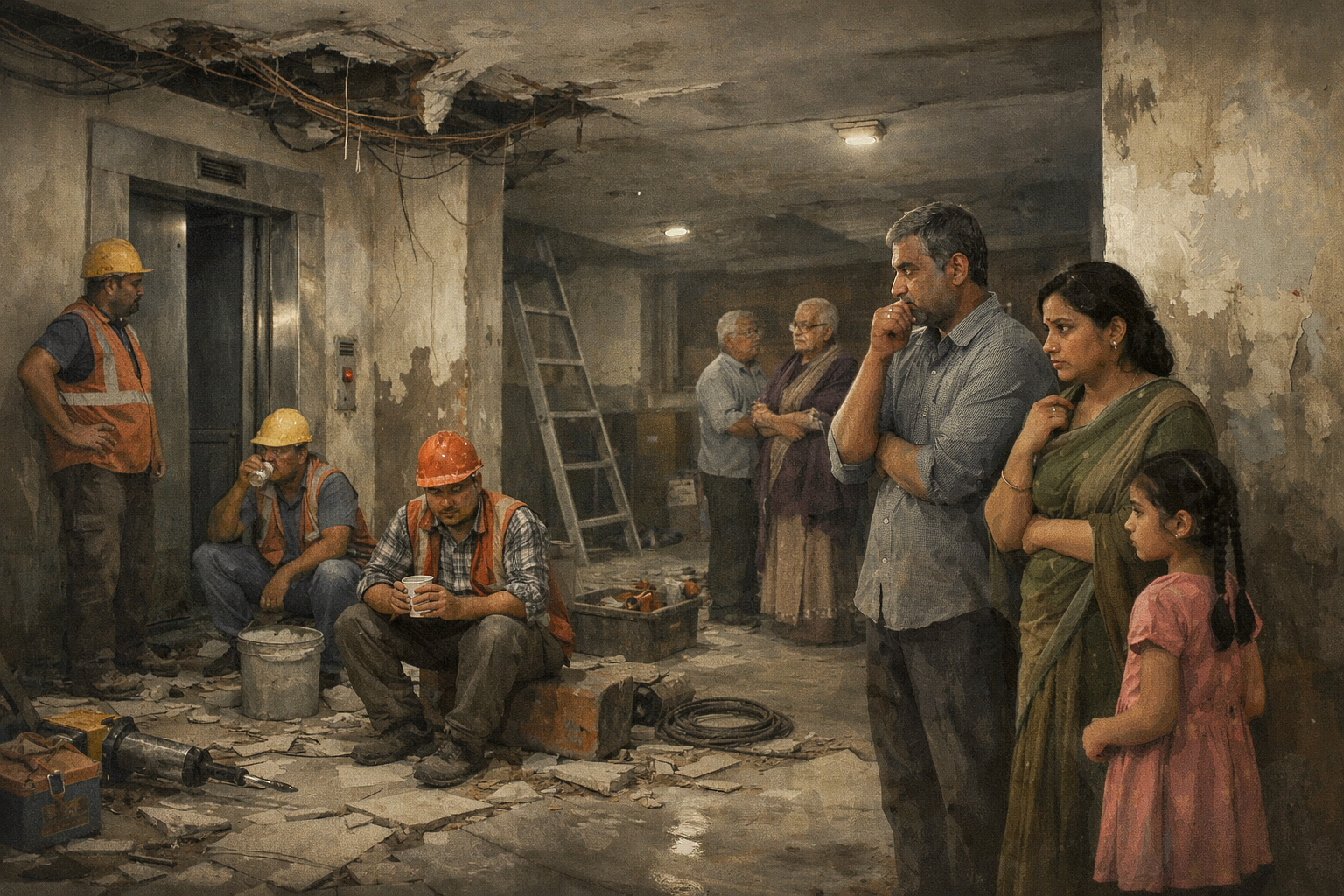

When Dhananjaya, a homeowner in a Bangalore apartment complex, noticed smoke billowing from the clubhouse on January 30, 2024, he had no idea this fire would expose a critical gap in India’s real estate protection framework. The blaze destroyed the ladies’ washroom and sauna facility, but what came next was even more alarming—the builder had failed to provide RERA mandatory insurance documents, leaving residents to bear the financial burden of repairs themselves.

This incident isn’t isolated. Across India, thousands of homebuyers are discovering that their builders have skipped a crucial legal obligation under Section 16 of the Real Estate (Regulation and Development) Act, 2016—leaving them financially vulnerable when disasters strike.

Understanding RERA Mandatory Insurance: The Basics Every Homebuyer Needs

RERA mandatory project insurance under Section 16 of the RERA Act requires all real estate developers to obtain comprehensive insurance coverage for their projects. This isn’t optional—it’s a statutory requirement designed to protect homebuyers from financial losses due to unforeseen events.

The insurance coverage mandated by RERA includes two primary categories:

- Title Insurance: Covers the land and building as part of the real estate project

- Construction Insurance: Protects against damages during the construction phase

According to the official RERA Act documentation, promoters must obtain all such insurances as notified by the appropriate government, pay all premiums before transferring insurance to the association of allottees, and hand over all insurance documents once the owners’ association is formed.

Why RERA Mandatory Insurance Matters

Without RERA mandatory project insurance, homebuyers face several critical risks:

Financial Exposure to Common Area Damages

Common areas—clubhouses, swimming pools, lobbies, elevators, and parking lots—represent significant value in modern residential complexes. A fire, flood, or structural failure in these areas can cost lakhs or even crores to repair. When builders skip RERA mandatory project insurance, these costs fall entirely on the residents’ association.

The recent Karnataka RERA ruling makes this crystal clear: builders cannot escape their statutory obligation to insure common areas of a housing project, even after handing over maintenance to an apartment owners’ association.

Legal Uncertainty and Repair Delays

Without proper RERA mandatory project insurance documentation, residents face months or years of legal battles to determine who’s responsible for repairs. In the Bangalore clubhouse fire case, restoration work remained stalled for months because insurance details were never shared with residents.

Hidden Liability Transfer

Many builders attempt to transfer insurance responsibilities to owners’ associations during handover, claiming they’re no longer liable once maintenance is transferred. This practice directly violates RERA mandatory project insurance requirements.

The Karnataka RERA Landmark Ruling: A Game-Changer for Homebuyers

Karnataka RERA ordered developers to submit all RERA mandatory project insurance documents within 30 days while partially allowing a complaint linked to the clubhouse fire. This ruling established several critical principles:

Builders Cannot Evade Insurance Obligations After Handover

Transferring maintenance to an owners’ association does not absolve builders of their RERA mandatory project insurance obligations. The promoter had not formed the association of allottees or transferred the common areas as required under RERA, and they also had not shared any insurance details under Section 16.

Insurance Documentation is Mandatory, Not Discretionary

Karnataka RERA reinforced that providing proof of insurance, premium receipts, and transfer documentation isn’t a courtesy—it’s a legal requirement under RERA mandatory project insurance provisions. Builders who fail to comply face penalties and may be ordered to pay for damages directly.

Residents Have Legal Recourse

The ruling empowers homebuyers to file complaints with RERA authorities when builders fail to provide RERA mandatory project insurance documentation.

How to Verify RERA Mandatory Insurance Before Buying Your Home

Smart homebuyers can protect themselves by conducting thorough due diligence on RERA mandatory project insurance compliance before committing to a property purchase.

Step 1: Check the State RERA Portal

Every state maintains an official RERA website where you can verify project registration and compliance status. According to property verification experts, you should:

- Visit your state’s RERA portal (e.g., MahaRERA for Maharashtra, K-RERA for Karnataka)

- Search by project name, builder name, or RERA registration number

- Review the project’s compliance status and uploaded documents

Step 2: Request Insurance Documentation Directly

Don’t rely solely on online portals. Ask the builder to provide:

- Original insurance policy documents covering both title and construction

- Premium payment receipts for the current period

- Details about coverage limits and what’s included

- Contact information for the insurance provider

Under RERA mandatory project insurance requirements, builders must make this information available to prospective buyers. Reluctance to share these documents is a major red flag.

Step 3: Verify the Insurance Provider

Contact the insurance company directly to confirm:

- The policy is active and premiums are current

- Coverage includes common areas specifically

- The policy will transfer to the owners’ association as required

- No gaps exist between different insurance periods

Step 4: Review the Sale Agreement Carefully

Your agreement for sale should explicitly mention RERA mandatory project insurance provisions, including:

- Builder’s commitment to maintain insurance until handover

- Clause confirming transfer of insurance to residents’ association

- Timeline for providing insurance documents

- Penalty clauses if insurance obligations aren’t met

According to RERA compliance guidelines, the promoter must pay all premiums and charges before transferring insurance to allottees.

What to Do If Your Builder Skipped RERA Mandatory Insurance

If you’ve discovered your builder hasn’t complied with RERA mandatory project insurance requirements, you have several remedies:

File a Formal RERA Complaint

Section 31 of the RERA Act allows aggrieved persons to file complaints against promoters for violations. Your complaint should include:

- Project details and RERA registration number

- Specific violation (failure to provide RERA mandatory project insurance)

- Supporting evidence (lack of documentation, refusal to share details)

- Relief sought (order to obtain insurance, compensate for damages)

RERA authorities can issue orders directing builders to comply within specific timeframes, backed by penalties for non-compliance.

Demand Insurance Documentation in Writing

Send a formal legal notice to the builder requesting all RERA mandatory project insurance documents within 15 days. This creates a paper trail useful for legal proceedings.

Coordinate with Your Residents’ Association

Collective action is more effective than individual complaints. Your residents’ welfare association should:

- Conduct a survey to determine if insurance documents were provided

- Gather evidence of the insurance gap

- File a joint complaint with RERA

- Consider engaging a real estate lawyer for association-level action

Consider Approaching the Appellate Tribunal

If RERA’s decision is unsatisfactory, Section 43 of the RERA Act allows appeals to the Appellate Tribunal.

Why RERA Mandatory Insurance Protects India’s Real Estate Market

Beyond individual homebuyer protection, RERA mandatory project insurance serves crucial market-wide functions:

Promotes Builder Accountability: When insurance is mandatory and enforceable, builders must maintain higher construction and safety standards. Insurance companies conduct their own inspections and risk assessments.

Protects Property Values: Properties with proper RERA mandatory project insurance maintain their value better because buyers know they’re protected against catastrophic losses.

Reduces Litigation and Disputes: Clear insurance coverage eliminates disputes about who pays for common area repairs.

Encourages Professionalism: RERA mandatory project insurance requirements separate professional, compliant developers from fly-by-night operators.

State-Specific Variations in RERA Mandatory Insurance Implementation

While Section 16 applies nationwide, individual states have implemented RERA mandatory project insurance requirements with varying levels of stringency:

Maharashtra (MahaRERA): Relatively strict enforcement of RERA mandatory project insurance, requiring detailed insurance disclosure on the MahaRERA portal. Builders must upload insurance certificates.

Karnataka (K-RERA): The recent Karnataka RERA ruling signals a more aggressive enforcement approach. K-RERA has made it clear that RERA mandatory project insurance obligations continue even after maintenance handover.

Uttar Pradesh (UP RERA): Has faced criticism for inconsistent enforcement of RERA mandatory project insurance provisions. Many projects lack insurance documentation.

Delhi NCR: Has multiple RERA authorities (Delhi, Haryana, UP), creating complexity. RERA mandatory project insurance enforcement varies significantly depending on which authority has jurisdiction.

Expert Tips for Homebuyers

While RERA mandatory insurance is crucial, comprehensive protection requires additional steps:

Conduct Third-Party Quality Audits: Before final payment, consider hiring an independent structural engineer to assess the property.

Verify Occupancy Certificates: These documents from municipal authorities confirm the building meets safety standards. No RERA mandatory insurance can compensate for a building that lacks basic legal approvals.

Review Builder’s Track Record: Research the developer’s history of insurance compliance in previous projects. Builders who’ve consistently maintained RERA mandatory insurance are more likely to do so in your project.

Join Buyer Groups Early: Connect with other buyers during the construction phase to collectively monitor RERA mandatory insurance compliance.

The Future of RERA Mandatory Insurance in India

As awareness grows and enforcement tightens, RERA mandatory insurance is likely to become even more central to real estate transactions:

- Several states are developing integrated platforms where buyers can instantly verify RERA mandatory insurance status online

- Future amendments to RERA may mandate additional insurance types for smart buildings or green-certified projects

- Regulators are expected to impose stricter penalties as more cases highlight the consequences of missing RERA mandatory insurance

- Banks may start considering RERA mandatory insurance compliance as a factor in project financing and home loan approvals

Conclusion: Your Rights Under RERA Mandatory Insurance

The RERA mandatory insurance requirement under Section 16 isn’t just legal jargon—it’s a fundamental protection that every homebuyer deserves. The Karnataka RERA ruling has reinforced that builders cannot shirk this responsibility, even after handing over common areas to residents.

As a homebuyer, you have the right to demand complete RERA mandatory insurance documentation before making your purchase. Don’t let builders deflect with vague assurances or claims that insurance is “being processed.” Verify everything through official channels, and don’t hesitate to file RERA complaints when builders fail to comply.

Informed buyers who insist on RERA mandatory insurance compliance are driving positive change. By exercising your rights and conducting proper due diligence, you’re not just protecting your investment—you’re raising standards for the entire industry.

Frequently Asked Questions (FAQs)

1. What is RERA mandatory project insurance?

RERA mandatory project insurance is compulsory insurance under Section 16 that protects homebuyers from paying for common-area damage.

2. How can I check RERA mandatory project insurance before buying?

Verify RERA mandatory project insurance on the state RERA portal, ask the builder, and confirm directly with the insurer.

3. What if my builder skipped RERA mandatory project insurance?

You can file a RERA complaint and legally demand RERA mandatory project insurance documents.

4. Does RERA mandatory project insurance end after handover?

No—RERA mandatory project insurance must be properly transferred to the residents’ association with documents.

5. What does RERA mandatory project insurance usually cover?

RERA mandatory project insurance typically covers fire, natural disasters, structural damage, and common-area risks.

(if you want to read more about other types of insurance, go here.)