Why Health Insurance Company Profits Confuse Policyholders

Health insurance often feels confusing to policyholders. Many people wonder: If insurance companies pay hospital bills, how do they still make profits? Are they relying on claim rejections, or is there a structured business model behind it?

The reality is more nuanced. Health insurance companies operate on data, risk management, and long-term planning—not denial tactics. Understanding how health insurance companies make money can help you make better decisions as a policyholder and avoid common misconceptions.

The Basic Business Model of Health Insurance

At its core, health insurance works on a risk-pooling model, a concept widely used in healthcare systems across the world.

According to the World Health Organization (WHO), risk pooling allows healthcare costs to be shared across a large population, reducing the financial burden on individuals during medical emergencies.

Source: https://www.who.int/health-topics/health-financing

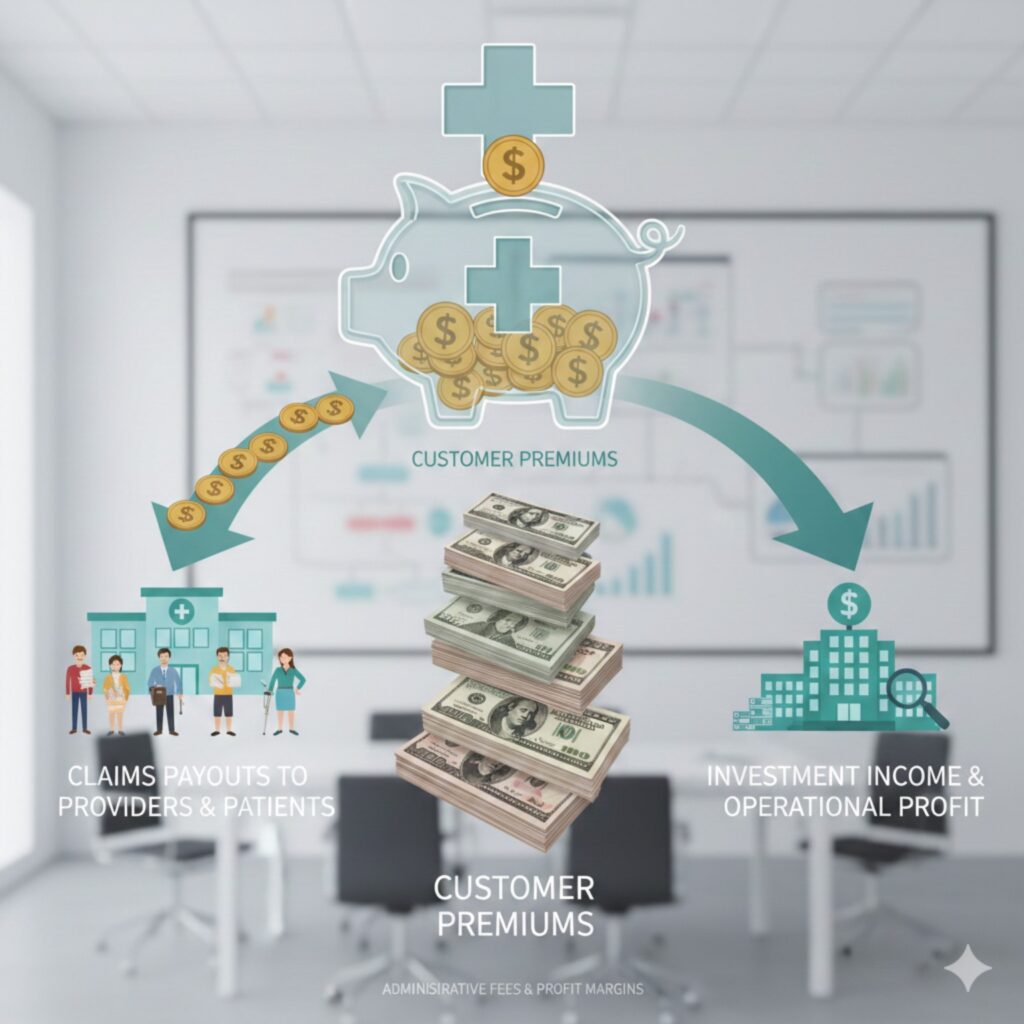

Major Ways Health Insurance Companies Make Money

1. Premium Collection: The Primary Source of Revenue

The most important way health insurance companies make money is through premium collection.

Most policyholders:

- Do not make claims every year

- Or make relatively small claims

This statistical balance allows insurers to function sustainably while continuing to pay legitimate claims.

2. Risk Assessment and Underwriting

Insurance companies carefully assess risk before issuing a policy. This process is known as underwriting.

In India, underwriting practices are governed and monitored by the Insurance Regulatory and Development Authority of India (IRDAI), which sets guidelines to ensure fairness and transparency in pricing.

Source: https://www.irdai.gov.in

3. Investment of Premium Funds

Another major income source is investment returns.

Health insurance companies invest premium funds in relatively safe, regulated instruments such as:

- Government bonds

- Treasury bills

- Corporate debt securities

These investments follow guidelines laid down by regulators and are influenced by India’s broader financial system, overseen by the Reserve Bank of India (RBI).

Source: https://www.rbi.org.in

4. Claims Ratio Management (Not Claim Rejection)

A common myth is that insurers make money by rejecting claims. In reality, excessive claim rejection damages trust and attracts regulatory scrutiny.

IRDAI regularly publishes health insurance statistics and claim settlement data, which insurers are required to disclose publicly. A claims ratio between 70% and 90% is generally considered sustainable in the Indian insurance market.

5. Policy Terms, Waiting Periods, and Exclusions

Health insurance policies include waiting periods and exclusions as part of standard risk management practices.

These rules are clearly outlined in policy documents and regulated by IRDAI to protect both insurers and consumers from misuse or misunderstanding.

6. Network Hospitals and Cost Negotiation

Insurance companies partner with hospitals to offer cashless treatment facilities.

These partnerships help control medical inflation—an issue highlighted frequently in India’s healthcare ecosystem, including in government-backed programs like Ayushman Bharat, administered by the National Health Authority (NHA).

7. Group Health Insurance vs Individual Policies

Group health insurance policies (such as employer-provided plans) work on larger risk pools and predictable demographics, allowing insurers to operate on lower margins while still maintaining profitability.

8. Long-Term Renewals and Customer Retention

Health insurance is a long-term business. Insurers often rely on renewals rather than short-term gains, which helps stabilize costs and improve service quality over time.

9. Operational Efficiency and Scale

Large insurers benefit from automation, fraud detection systems, and data analytics. This operational efficiency reduces administrative costs per policy and supports sustainable profits.

Are Health Insurance Profits Regulated in India?

Yes. Health insurance companies in India are strictly regulated by IRDAI, which enforces rules related to:

- Solvency margins

- Investment limits

- Consumer protection

- Claims transparency

This regulatory oversight prevents unchecked or unethical profit-making.

Final Thoughts on How Health Insurance Companies Make Money

Health insurance companies are businesses, but their profits come from risk pooling, pricing accuracy, investment income, and efficiency, not from denying genuine claims.

Understanding this structure helps policyholders set realistic expectations and use health insurance as a financial safety net rather than a short-term transaction.

FAQs: How Health Insurance Companies Make Money

Do health insurance companies profit if they pay claims?

Yes. Paying claims is part of their business model. Insurers profit as long as total claims remain within expected limits based on premiums and investment income.

Is claim rejection the main source of profit for insurers?

No. Claim rejection harms trust and regulatory standing. Insurers focus on balanced claims ratios, not denial tactics.

How do investments help insurance companies earn money?

Premiums are invested in safe, regulated instruments. Returns from these investments contribute significantly to overall profitability.

Why do policies have waiting periods and exclusions?

These terms help control risk, prevent misuse, and keep premiums affordable across the risk pool.

Are health insurance companies allowed unlimited profits in India?

No. IRDAI regulates pricing, investments, and solvency, ensuring profits remain within ethical and legal limits.